Do Investors Put Too Much Stock in the US?

Summary: Investment advisors typically recommend that you put somewhere between 50% and 75% of your stock investments into US stocks and the rest into international markets. Most individual investors have 70% or more of their stock money in the US or their home country, a phenomenon that’s aptly called home country bias. But there are reasons to believe that even 50% is too much.12

Disclaimer: I am not an investment advisor and this is not investment advice.

Published 2017-03-26; last updated 2026-01-24.

A note from 2026: US equities handily beat international equities from 2017 to 2025. I still believe the arguments I originally wrote are mostly correct, although I was overconfident about their strength; and there was a good justification for home country bias that I wasn’t aware of, namely, expropriation risk.

I originally wrote that US investors might want to invest only 0–30% in US stocks. I now believe that’s taking it too far. I believed that the strongest argument for under-weighting US stocks was income diversification, but the correlation between domestic equities and personal income isn’t high enough to justify a 0% weighting.

Although I was overconfident in 2017 and wrong about some things, I believe I was correct to criticize most justifications for home country bias, and I don’t believe US equities’ subsequent outperformance was predictable ex ante; see Asness, Ilmanen & Villalon’s International Diversification—Still Not Crazy after All These Years (2023).

Contents

- Contents

- The global market portfolio

- Why you might overweight international stocks

- Good justifications for home country bias

- Other common justifications for home country bias, and why they’re wrong

- Conclusion

- Changelog

- Notes

The global market portfolio

Let’s start from the efficient market hypothesis.3 That means the prices of financial assets fully reflect their intrinsic value. In an efficient market, there’s only one “free lunch”: diversification. If you don’t own a globally diversified portfolio, you’re taking on unsystematic risk, and you could reduce your risk by diversifying.

If we take this to the limit, how do we get the most diverse possible portfolio? Simple: buy some of every asset in the world. In particular, buy each asset in proportion to its total market value. That would give your portfolio something like 20% US stocks, 20% international stocks, 50% bonds, and 10% real assets such as gold and real estate.

If we look at just the stock portion of your portfolio, you’d have 60% in US stocks and 40% in foreign stocks (as of 2024—these percentages will likely change over time). So if we simply follow the efficient market hypothesis, we should aim for about a 60/40 split.

Not everyone buys this. Here’s a quote from the popular personal finance blogger Mr. Money Mustache:

What about International stocks? Some people like to get fancy and buy international index funds, which can do well when the US is hurting (as it has been recently). This is fine, as long as you understand that it’s just another form of trying to outsmart the basic stock index. When you do this, you are stating that you believe the stock markets of the other countries are more undervalued relative to future growth, than the US market is.

But that’s exactly the opposite of how it should work! You don’t start with 100% investment in US stocks and then require justification for diversifying globally. If you accept the efficient market hypothesis, you should start with the global market portfolio and demand a justification for deviating from that—and a disproportionate allocation to US stocks qualifies as a deviation. You should buy the whole world instead of privileging the United States over other countries.

Why you might overweight international stocks

If you buy the global market portfolio, you will have about half your stocks in the US and half in other countries. But we have several convincing reasons for decreasing our US allocation and buying more stocks in foreign countries.

Income diversification

You don’t only depend on your investments to get by. You probably have a job, and if not, you probably will have one at some point in the future.

If you work in the United States, your salary moves up and down for many of the same reasons that the US stock market moves up and down (and similarly if you live and work in any other country). If a big recession hits, the US stock market could lose most of its value and you could lose your job. You can think of your job as a major human-capital investment into the United States, and you should take that into consideration when you’re deciding how to allocate your monetary investments.4

If you want to be precise, you could estimate how much money you will put into savings throughout the your future career and consider that as part of your investment portfolio.5 Then take that into account when determining what your allocation should look like.

For example, if you currently have $500,000 in savings and you estimate the discounted value6 of your additional future savings at $500,000, you might invest $100,000 into the US market and the rest into foreign countries (perhaps including bonds as well as stocks). That way you’ll have a 60/40 allocation to US/international after accounting for the future value of your career earnings.

Most people below the age of maybe 40–50 will deposit a lot more money into their savings throughout their career than they have right now—most of their money will come in the future. The book Lifecycle Investing uses this fact to argue that young people should leverage their investments. You could make a similar argument that young people should leverage their international investments in particular. I won’t go into the specifics of this argument, but Lifecycle Investing discusses similar topics, so it’s a good read if you want to think more about this.

Two important caveats:

- Your future income does not perfectly track the US stock market, so you still get diversification benefits from investing in US stocks along with international stocks.

- The “income diversification” argument for under-weighting US stocks only applies if you still have a long career ahead of you. If you’re retired or close to retirement, you might prefer to fairly-weight US stocks with respect to the global market portfolio, and possibly currency-hedge your international holdings. You might even want to over-weight US stocks in this case, as a hedge against future expenditures (see below).

Valuation

Although we started with the assumption that you can’t beat the market, we can actually find a few cracks in the efficient market hypothesis. One such crack is the value premium: cheap companies (as measured by price to earnings, price to book, or some similar price-to-fundamental ratio) outperform expensive companies in the long run.

This applies across countries as well: cheap countries tend to outperform expensive ones.7

Star Capital has a site comparing countries on several valuation metrics. No matter what metric you choose, the United States looks expensive relative to most other countries in the world, which suggests that it will probably see weaker returns over the next few years than the world as a whole. As of 2025, Research Affiliates predicts that US stocks will have real returns of about 2% per year over the next 10 years, compared to 6% for developed ex-US markets and 7% for emerging markets. That said, Research Affiliates’ projections may give too much consideration to valuation.8 AQR’s capital market assumptions, which are much more conservative about incorporating valuations, project a 4.2% return for US equities vs. 4.9% for developed ex-US—a much smaller difference, but still a difference. These forecasts could be wrong—we can’t perfectly predict what markets are going to do—but it’s a good bet that the US will perform poorly compared to the global stock market.

The United States represents about 60% of the global stock market right now, but if the market were fairly valued, it would probably represent a substantially smaller fraction. There’s no single way to decide what the US market’s “true” valuation should be, but one reasonable approach is to use GDP weighting. The United States represents about 25% of global GDP, so we could put 25% of our stock investments into the US and 75% into the rest of the world.

I haven’t given a serious justification for why value investing works because that wouldn’t fit in this essay. For more, see the book Global Value by Meb Faber.

Account restrictions

In some cases, some of your money may have restrictions on how you can invest it. For example, if you have a 401(k) plan with your employer, you can only put money into the funds that your employer provides. A lot of the time, these funds don’t give you a lot of options when it comes to international holdings. (My own 401(k) provider gives seven choices for investing in US stocks or bonds, and only one choice for investing internationally.) If that’s the case, perhaps you should put your restricted accounts into US assets, and invest relatively more of your discretionary money into other countries to balance things out.

Do be careful about this—you could end up in a situation where your regular brokerage account declines a lot while your 401(k) stays stable, but you can’t withdraw from your 401(k) without paying a penalty. Sometimes that’s a risk worth taking, but be aware that it could happen.

Good justifications for home country bias

Retirement spending

If you’re retired or otherwise expect to spend more money than you earn, then you want to hedge against your future expenditures. You should overweight assets that you expect to go up in value when your spending goes up, and your spending is more correlated with your country’s stock market than with other markets. Extending this reasoning, you should hedge not just the country you live in but the specific expenditures you expect to have. For example, if you own a home, then you’re exposed to fluctuations in housing prices.

Expropriation risk

If you invest in a foreign country, there’s some risk that the country will expropriate your holdings and you’ll never get them back.

There is a corresponding risk that your local country will confiscate your money—this tends to happen after communist revolutions. But expropriation risk is probably a bigger concern.

Expropriation Risk and Return in Global Equity Markets (2002)9 estimated the magnitude of risk. It found nearly zero expropriation risk premium in developed countries (see Table 4 under “Sample Selectivity”), but a 6% annual risk premium for emerging markets. If the paper’s results are correct, then expropriation risk does not dampen my enthusiasm for diversification across developed markets, but it does make emerging markets look riskier.

A 2012 World Bank report10 came to a similar conclusion. It looked at the history of expropriation events and found that they occurred disproportionately in emerging economies, and particularly in repeat offenders.

Other common justifications for home country bias, and why they’re wrong

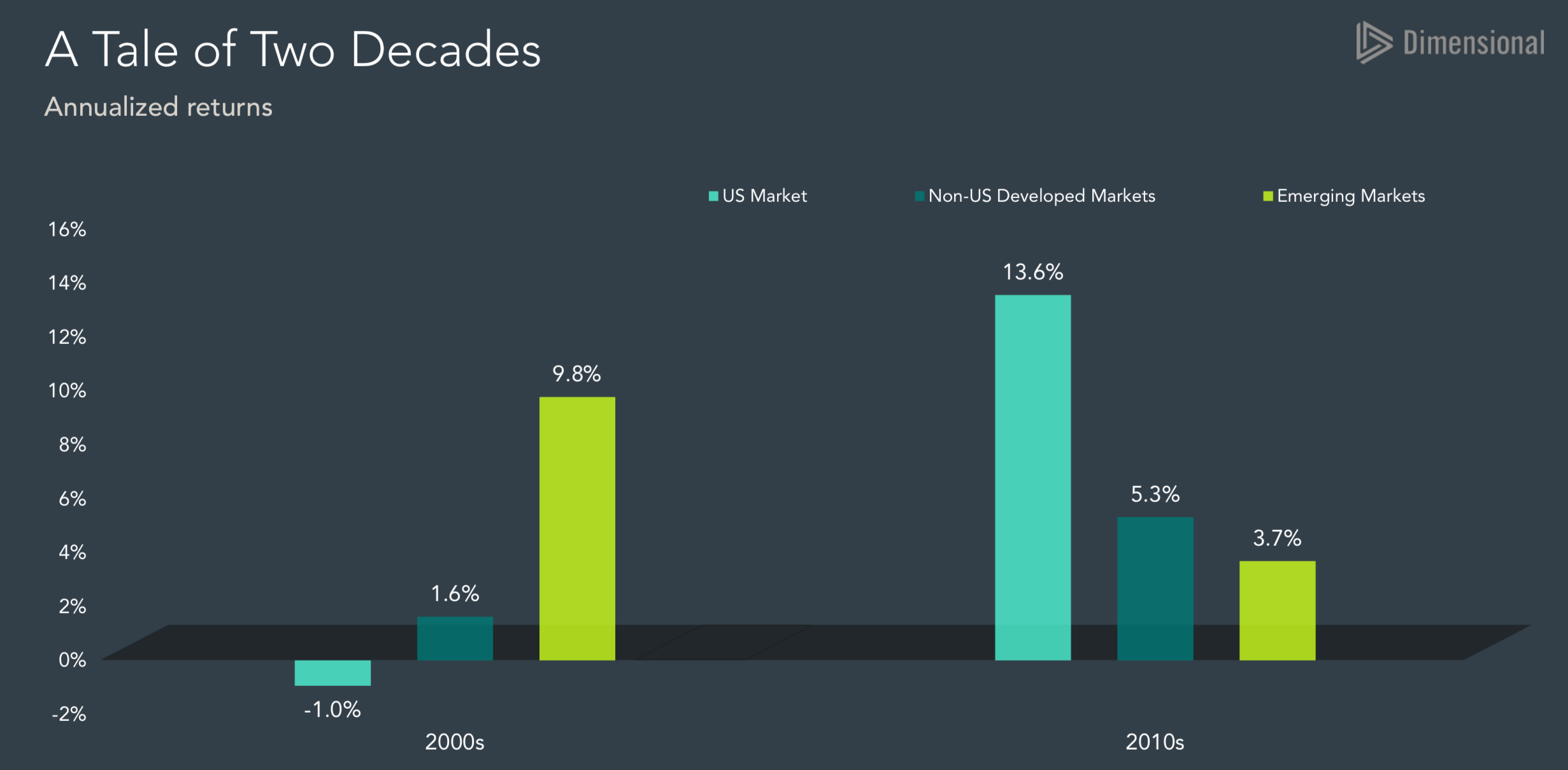

“The US market outperforms other countries’ stock markets.”

I will let this chart speak for me: (credit to Dimensional Fund Advisors)

“The United States is a big country.”

(This one only works if you live in the US; residents of other countries don’t have this excuse.)

The United States represents a big chunk of the global market cap, so you could maybe justify holding about 40-60% of your stock investments in the US on that basis. But even then you still couldn’t justify holding 70+% of your stock investments in the United States, as many people do.

“Many US companies sell their products globally, so you already get international diversification by holding US stocks.”

While it’s true that US companies with a global presence provide diversification benefits that you don’t get from local companies, you can get even better diversification by holding stock in foreign companies. Even if your portfolio is sort of diversified, that doesn’t mean you shouldn’t build a portfolio that’s even more diversified. You shouldn’t limit yourself without a good reason.

Historically, international stocks have not been perfectly correlated with US stocks, so you could have gotten a better risk-adjusted return by investing in both. See Vanguard (2019), Global equity investing: The benefits of diversification and sizing your allocation.

“I should buy what I know.”

People often argue that they understand the United States, so they should buy the companies that they understand. (Or they take this a step further and say they should buy the industry that they work in.) While it’s true that they probably do understand some companies better than others, the problem is that everyone else does too. There are plenty of people in the market who know more than you do even about your area of expertise, so you should not usually expect to find undervalued stocks in an area just because you understand it. The real question is, do you understand it better than the hedge funds who research their investments full time? Which you don’t. So you probably can’t rely on this excuse.

“The United States has the strongest economy in the world.”

Every reasonable investor knows that the United States has a strong economy. If people believe the US stock market will perform better than other countries’ markets, smart investors in other countries will pour money into the US until it stops being underpriced. (We can see that this has already happened: the United States accounts for 25% of world GDP, but 60% of the global market cap, which means the market already expects the US to perform well.) You can’t outperform the global market by buying US stocks, because the strong economic growth is already factored in to the market valuation.

If anything, you should invest in countries that have relatively weak economies. People tend to put too much money in strong economies and not enough money in weak ones, so weak economies are underpriced on average and you can make more money by putting money into them.7 “Underpriced market” and “weak economy” don’t always mean the same thing, but they often align.

“Investing internationally exposes you to currency risk.”

Usually, if you buy international stocks, you have to buy them in that country’s local currency. That means you face a risk that exchange rates could move against you.

This is not a serious concern, for several reasons:

- Historical studies on international investing typically don’t hedge currency, and they still find large benefits to diversification. For example, see Vanguard (2019) cited previously.

- Exchange rates tend to fluctuate much less than equity prices, so they contribute relatively little to the overall risk of a portfolio. See the CBOE volatility indexes (e.g., compare US/Euro exchange volatility EVZ versus EAFE equity volatility VXEFA). Vanguard (2019) also addresses this, under the heading “Impact of currency exposure”, and finds that currency hedging only slightly decreases the volatility of a portfolio, and in some cases actually increases it.

- If you still prefer to avoid foreign exchange risk, you can buy a currency-hedged international equity fund (such as DBEF). You will probably end up paying a little more in fees, but the fees are dwarfed by the diversification benefits of investing internationally.

Conclusion

Most people put way too much money into US stocks. More than that, conventional investment advice too heavily favors US stocks over international stocks. Non-retired Americans may not want to hold more than 60% of their stock investments in the US. We should probably hold less than that if our salary is tied to the US economy; and we should probably hold less still because the US stock market appears overvalued relative to other global markets.

Changelog

- 2024-03-28: Add argument “The United States has the strongest economy in the world.”

- 2024-04-24: Update numbers for US vs. international market cap and GDP because the numbers from 2017 are now somewhat inaccurate.

- 2024-05-08: Embed an image of a cool chart I saw.

- 2025-05-05:

- 2026-01-24: Add a note about how I have and haven’t changed my mind since originally publishing this.

Notes

-

If you don’t live in the United States then most of the reasoning in this essay applies to you in the same way, and the rest of it applies even more strongly. US investors can at least sort-of justify putting lots of their money in the US based on the fact that it covers a huge chunk of the global market capitalization, but people in other countries can’t make the same excuse. ↩

-

This post mostly talks about people’s stock investments, and not their overall investment portfolios. We could perhaps argue that people also ought to hold more foreign bonds or foreign real estate. I believe this is true. But it’s probably not as important, and it introduces some complexities into the argument, so it’s beyond the scope of this essay. ↩

-

We have some good reason to doubt the efficient market hypothesis, but even so, it makes sense to assume markets are efficient as a starting point and go from there. ↩

-

For the same reason, you may want to avoid investing in the same industry that you work in. For example, if you work at Ford, you might not want to put any money into automobile stocks. ↩

-

The book Lifecycle Investing uses this concept to argue that young people should leverage their investments. Another book, Are You a Stock or a Bond?, explores the concept in more detail, although I haven’t read it. ↩

-

You need to apply time discounting to your expected future earnings. Having $100 twenty years from now doesn’t count for as much as having $100 today. So when I talk about having a discounted value of $100, I mean that you expect to have some amount of money in the future that’s worth as much as $100 today. The discounted equivalent of $100 today might be $105 a year from now, or $250 twenty years from now. ↩

-

Meb Faber. Global Value: How to Spot Bubbles, Avoid Market Crashes, and Earn Big Returns in the Stock Market. ↩ ↩2

-

They assume valuations will fully mean-revert after 20 years (source), which reflects historical trends, but it may be too strong an assumption. ↩

-

Dahlquist, M., & Bansal, R. (2002). Expropriation Risk and Return in Global Equity Markets. ↩

-

Eden, M., Kraay, A., & Qian, R. (2012). Sovereign defaults and expropriations: empirical regularities. World Bank Policy Research Working Paper, (6218). ↩