Value Investing in the Age of AGI

Introduction

Most people who write about AI and investing fall into one of two camps: traditional investors who see the high valuations of AI stocks and say it’s a bubble;1 or AGI-pilled investors who will buy AI stocks at any price, regardless of fundamentals. There’s only a tiny intersection of people who understand that AGI is not a normal technology while also recognizing that fundamentals matter.

I’m not an expert (or even a journeyman) on AI or fundamental analysis, but I do know a little bit about both.

The basic thesis of value investing is that the market over-rates expected future growth and under-rates present-day fundamentals. Stocks that are poised to benefit from AGI tend to be growth stocks—people have high expectations for them, and they’re priced expensively relative to present-day fundamentals. That suggests that we shouldn’t buy AI-related stocks.

At the same time, the market does not appear to expect AGI, which suggests we should buy them. Which of these two forces is stronger?

My current thinking is that value investing probably won’t work in light of AGI, but there is some reason to believe it might work even better; and value investing is a useful hedge in case AI progress slows.

Updated 2026-03-13 to replace the value spread chart with a more relevant one.

Contents

- Introduction

- Contents

- The value spread vs. AGI

- Defenses of value investing

- Value investing as a hedge against long timelines

- Notes

The value spread vs. AGI

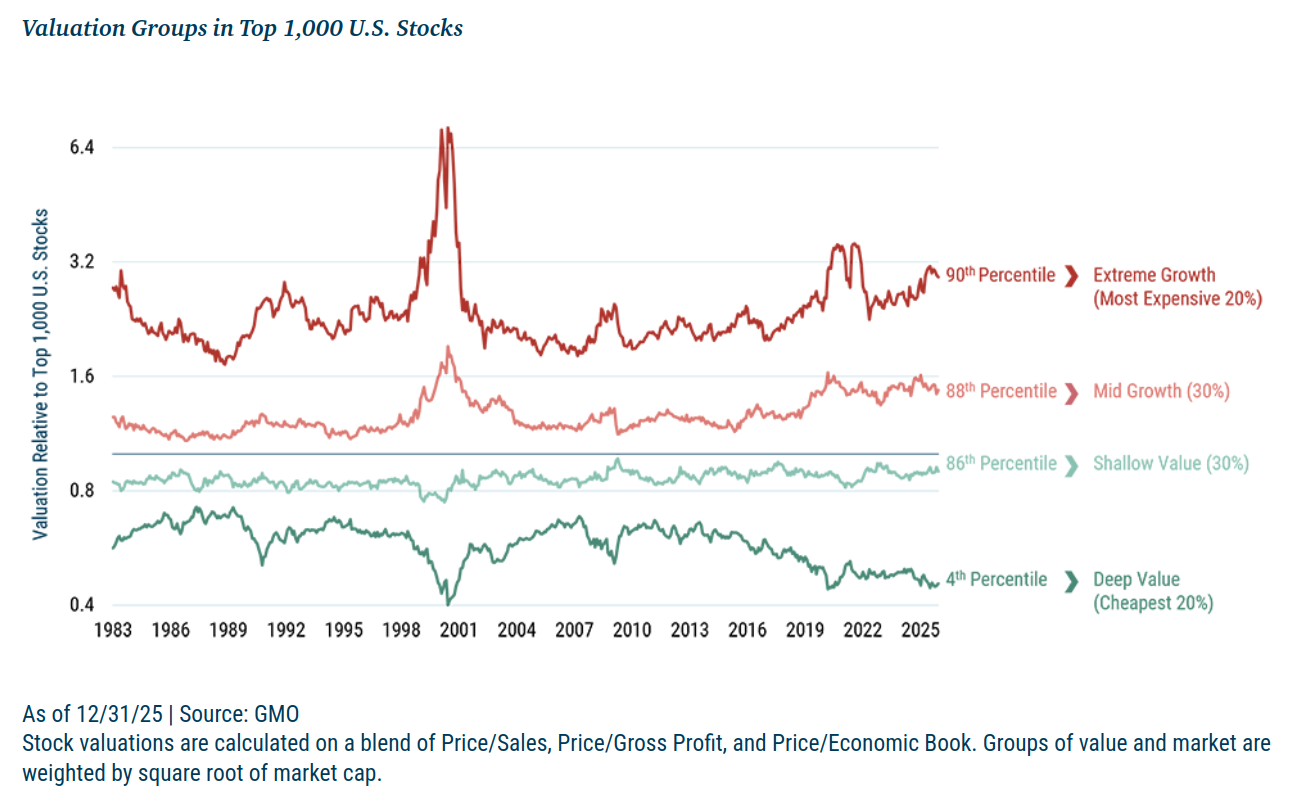

source: GMO

Right now (in early 2026), the valuation spread between US growth and value companies is large relative to history. This is by both the value and growth sides: value stocks are historically cheap, and growth stocks are historically expensive. Growth stocks may experience a crash like they did after the dot-com bubble.

However, the crash might never come because we might be living through the final market cycle. The development of AGI in the next decade could end the economy as we know it.

Civilization is on track to develop AGI within the next decade, and ASI may follow soon after.2 When ASI arrives, our investments probably won’t matter anymore, for one of several reasons:

- ASI will be misaligned and it will kill everyone. (This is the most likely outcome.)

- ASI will be aligned, and it will be so radically good for the economy that nobody will care about money anymore.

- A small set of people will use aligned ASI to take over the world and leave everyone else at the mercy of their whims.

There is some chance that none of those things will happen. Even if they do, there may be a meaningful transition period where AI is powerful enough to replace a significant fraction of human labor, but not yet powerful enough to kill everyone. In those scenarios, it matters how we invest. We can then spend our investment returns on reducing the odds that ASI kills everyone.

In the scenario where AI transforms the economy but doesn’t (yet) render money useless, will value investing work?

My best guess is no. Right now, the market is sending the signal that AI is a useful ordinary technology. The market appears to be pricing Nvidia the way it priced Cisco in the late 90’s: “[AI/The Internet] will be the next big thing. [Nvidia/Cisco] manufactures the infrastructure that [AI/The Internet] relies on; it is well positioned to make huge profits.”

(Cisco had a Price/Sales ratio of 21 at the end of 1999, and 38.9 at its peak in March 20003; Nvidia’s Price/Sales is 25.1 as of the beginning of 2026.)

If AI is not a normal technology, and it comes to dominate the world economy, then AI stocks’ current prices appear too low. Current valuations imply strong growth, but not radical growth.4 In a world where AI replaces half of all human jobs, Nvidia’s revenue could comfortably reach $60 trillion, in which case its current price is much too low.

How Nvidia's revenue could reach $60 trillion

Some back-of-the-envelope math:

- World GDP is ~$120 trillion. If AI can do half of human jobs, that could double world GDP to $240 trillion. (That’s not really how it works, but I’m keeping it simple.)

- AI companies would be willing to spend perhaps half their revenues on data centers, or $120 trillion.

- Historically, about half the cost of data centers has gone to GPUs, implying $60 trillion of revenue for Nvidia, assuming Nvidia can maintain its near-monopoly on AI hardware.

If economic growth accelerated across the board, all else equal, that would be bad for the value factor. As a simplistic illustration, suppose the market expects value companies’ earnings to grow 5% next year, and growth companies’ earnings to grow 10%. Value investing works when the market’s expectations are overconfident, and earnings growth reverts toward the mean. If value and growth companies’ earnings grow by 6% and 9% respectively, then the earnings of the value factor will beat expectations by 2 percentage points. However, if AI doubles every company’s earnings growth, then value and growth companies will grow earnings by 12% and 18%, respectively. Even though earnings growth still mean reverts, the value factor underperforms expectations.

The same information presented as a table:

| Scenario | Value Co. Growth | Growth Co. Growth | Value Outperformance |

|---|---|---|---|

| market expectation | 5% | 10% | 0% |

| mean reversion | 6% | 9% | 2% |

| AI acceleration + mean reversion | 12% | 18% | -1% |

Defenses of value investing

I see two ways that value investing might still work in light of AGI: competition increases and AI makes predictions harder.

The first argument: Competition may increase.

Current market prices are baking in an expectation that today’s winners will stay winning. Right now, Nvidia effectively has a monopoly on AI hardware. But other companies are trying to change that. AMD, Nvidia’s main competitor, is working hard to catch up on AI; Amazon, Google, Meta, and Microsoft are all building their own AI chips; and a handful of startups are trying to compete as well.5 If some of those companies succeed, Nvidia’s market share and profit margin may not be good enough to live up to the market’s expectations.

The second argument: AI makes it harder to predict the future.

It is notoriously difficult to predict which problems are easy or hard for AI. Therefore, it is difficult to predict which industries will most benefit from advancements in AI capabilities. When you don’t know which companies will experience the most earnings growth, you want to hold the companies that have a lot of earnings right now.

Example:

If Gale’s Growth Inc. (GGI) has a P/E of 20 and Vicky’s Value Co. (VVC) has a P/E of 10, that means the market is willing to pay a premium for GGI because it expects GGI to have stronger earnings growth in the future. Increasingly-powerful AI bolsters both companies, and it becomes very hard to predict whether GGI or VVC will benefit more. In that situation, I’d prefer to own VVC because I’m buying the same amount of earnings at half the price.

In other words, if I have equal growth expectations for GGI and VVC, then I’d prefer VVC. Right now, the market expects GGI to have better growth, but AI advancements could throw a wrench in the market’s expectations.

Quoting Matt Levine:6

With a sufficiently general-purpose technology it’s not clear whether the value will mostly accrue to the builders of that technology or to its users. But surely it is at least plausible that AI will mostly make its users richer, so the way to bet on AI is mostly to bet on regular, non-AI companies that don’t use it yet but eventually will.

An alternative possibility (raised by AI 2027 and Bayesian Investor) is that once AI agents become sufficiently advanced, frontier AI developers may stop releasing the agents and keep the benefits to themselves. If that happens, the economic benefits of AI may simply accrue to the AI developers. That would be bad for value stocks, but it would also have such a warping effect on the economy that it’s hard to say what the right response would be.

Value investing as a hedge against long timelines

AI timelines might lengthen for various reasons. Maybe AI advancement hits a wall; maybe an economic recession makes it too hard for AI companies to get capital investments; maybe training new LLMs simply becomes too expensive and companies can’t raise enough money; maybe governments wake up to the existential danger of ASI and start imposing strong regulations; etc.

My guess is none of those things will happen. But they’re not terribly unlikely, either. Any event in that genre seems like it would be good for value stocks and bad for growth stocks. At minimum, if AI capabilities slow down, the lofty valuations of AI-related stocks will start looking too optimistic, and prices will likely come down. Value stocks are something of a safe haven protecting against valuations crashing back to earth (I say “something of” because in the investing world, nothing is ever guaranteed to be safe).

I’m less bullish on value investing than I was five years ago, but I still keep about a third of my money in value stocks. I expect them to outperform if AI timelines are long, and there’s some chance they outperform even if AGI arrives soon.

Notes

-

Vanguard did better than most7: in their December 2025 market outlook, Vanguard rightly predicted that the future is likely to be very bad or very good, while “average” outcomes are unlikely. But they didn’t quite get it. They wrote that transformative AI could cause real GDP growth to surge from the historical 1–2% up to…3%. Really, Vanguard? The development of an artificial alien species that intellectually surpasses the smartest humans would increase GDP growth to 3%?

I’m only picking on Vanguard because their take on AI was better than the other takes I read from the big investing firms. In general, Vanguard is arguably the respectable investing company—they’ve probably done more for retail investors than anyone else. ↩

-

I think of AGI as an AI that’s smart enough to replace most human workers, and ASI as an AI that’s smart enough to outsmart all of humanity put together—as in, if it resolved to kill us all and we resolved to live, then we would die and it wouldn’t be close.

It’s possible that AGI and ASI aren’t that different, and it’s possible that ASI would have to be much more advanced than AGI. ↩

-

Fiscal year 1999 revenue was $12.15 billion according to a Cisco press release. At the end of 1999, Cisco’s market cap was $253 billion (source).

According to a secondary source, Cisco’s Price/Sales peaked at 38.9 in March 2000. ↩

-

I spent a while trying to come up with a model for what growth expectations are implied by AI-related companies’ valuations, but it got too complicated so I gave up. I’d still like to see a good fundamental analysis of what stocks ought to be worth in light of AGI, but I’m not going to be the one to do that analysis (at least not today). ↩

-

For references, see this Claude chat. ↩

-

Levine, M. (2025). Hedge Fund AI Is Cheap AI. ↩

-

Vanguard Research (2025). Vanguard economic and market outlook for 2026 – AI exuberance: Economic upside, stock market downside. ↩