Reading Notes

Preamble

This page contains my reading notes on most important articles I've read since 2015. I take notes on articles I want to remember.

You can click on a tag to show only notes with that tag, and click the tag again to show all notes.

Most of the time, first-person pronouns in my notes refer to the author of the book/article, not to me. Lines preceded by "me:" give my own thoughts.

Disclaimers:

- I primarily write these notes for my own benefit, so some parts might not make sense. But I hope you find something useful in them.

- Unless otherwise specified, these notes represent my interpretation of the authors' views, not my own views. But also I can't promise that I understood the authors' views correctly.

- I exported my notes from org-mode to HTML with minimal editing. Some things might not look right.

Readings

Dynomight: My advice on (internet) writing, for what it's worth

https://dynomight.net/writing-advice/

- Make something you would actually like

- Nobody really understands anyone else. You can't predict exactly what other people would like. But you can predict what YOU like

- My blog is weird because I like weird

- But your brain is lying to you. If someone else wrote your post, would you actually like it?

- If you run out of ideas, just take one of your old ones and do it again, better. It's fine, I promise

- Editing exercise: Go through and circle the good parts. Then delete everything else

- Be funny, maybe. You fuckers all take yourselves too seriously

- But humor needs to be worth it (short jokes are cheaper than long jokes)

- Write for your allies, not your haters

- Clear writing is next to godliness. But the optimal number of confused readers is not zero

- Some writers get bogged down in doing new research. But if you already believe something, then either you have good reasons, or you don't. Just explain why you believe it

Some things I noticed while LARPing as a grantmaker causepri

(abridged notes)

- You should probably be like I do research to figure out what projects should exist, then make them exist rather than I evaluate the applications that come to me

- Winner's curse: If you're more excited about X than your peers, that's evidence that X is not as good as you think

- Fear theories of change that route through "empower this sketchy person and hope they do good things"

- me: There's a conflict between winner's curse and the neglectedness heuristic

- Perhaps an important discriminator is: Can you identify a reason why others under-rate this intervention?

Willingness to look stupid is a genuine moat in creative work self_optimization

https://sharif.io/looking-stupid

- Richard Hamming: Nobel Prize winners stop doing great work after they win the prize because they're trying to find the next big thing, instead of planting the little acorns from which mighty oak trees grow

- Many good ideas come from young and unproven people. I don't think young people are smarter than old people, or work that much harder; but they're not afraid of looking stupid

- HN: Young people do worry about looking stupid, they just don't know that they look stupid

- We wanted to write something clever on a birthday cake. We decided "Let's say a bunch of ideas out loud so we can get to the good ones." And it worked!

- Evolution lets mutations get locally worse, and sometimes they get globally better. If evolution had a sense of shame, it wouldn't work

- The trick is don't try to share something good. That's a game you can lose, and you won't want to lose. Instead, play the game of sharing something at all

Rational Reminder: Should gold and other metals be considered in portfolio allocation? finance

summary of best comments from https://community.rationalreminder.ca/t/should-gold-and-other-metals-be-considered-in-portfolio-allocation/13250

- Gold has worked as an inflation hedge over multi-century time horizons. Gold in Ancient Rome could buy a similar amount of goods as gold today. But gold is not a good inflation hedge even over 50-year horizons

- Golds are not a replacement for bonds. The defining characteristic of Treasury bonds is that they provide predictable cashflows (or even real cashflows if you buy TIPS). Gold's price is volatile and there is no strong reason to expect positive real returns

- 1975–2001 gold declined 60% after inflation. "A good store of value does not have 60% losses in purchasing power over long-term investment horizons"

- Jastram (1977): Over 400 years of history, gold made for a poor inflation hedge. During inflationary periods between 1933 and 1967, gold performed worse than a commodity index

- Erb & Harvey (2013): "While gold might protect against inflation in the very long run, 10 years is not the long run. In the shorter run, gold is a volatile investment which is capable and likely to overshoot or undershoot any notion of fair value."

- They found that gold exhibits some mean reversion when it is above or below the long-run average real price

- F&F: Owners of gold jewelry earn a "consumption dividend" (i.e. they benefit from using the gold as well as owning it). If gold is correctly priced, then investors who don't earn the consumption dividend should prefer not to hold gold

- People make the mistake of comparing the historical 0.7–1% real return on gold to the present-day [as of 2021] <1% yield on bonds. But gold doesn't look so good when you notice that bonds had a long-run real yield of 1.6%

- If you take an asset with completely random returns and replace some of your equities with it, and look at the portfolio during the worst period for equities, it will necessarily look better than the 100%-equities portfolio

- In the UK, gold had >50% real drawdowns 1562–1592, 1738–1801, and 1897–1920 (source: The Golden Constant (book))

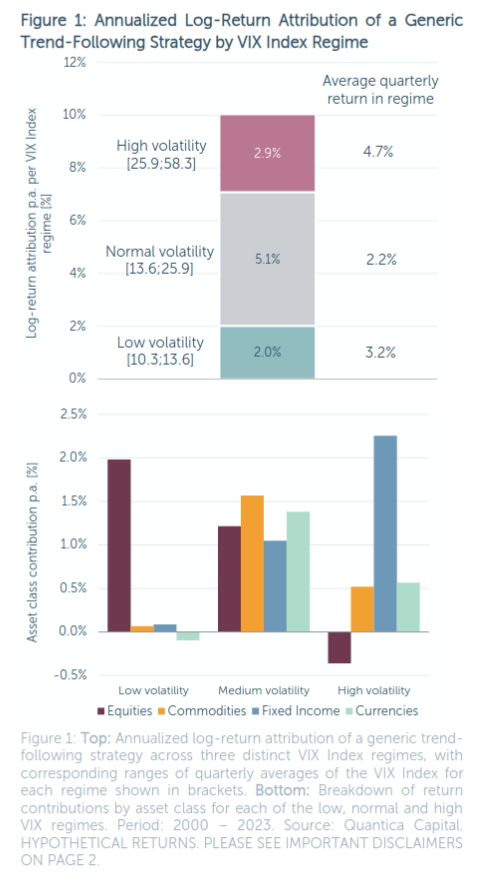

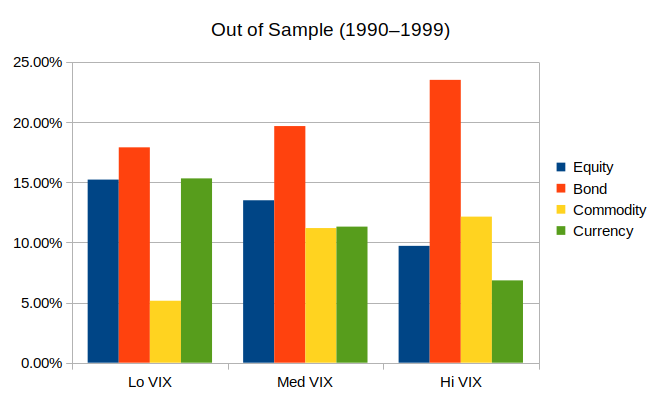

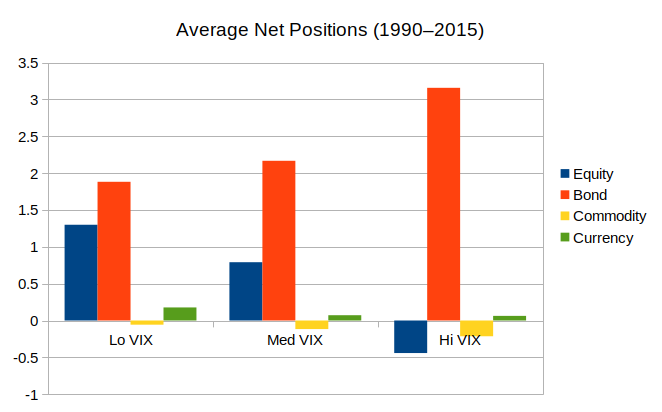

Quantica: Are Trendfollowing CTAs Truly Long Volatility? (2023) finance trend

https://quantica-capital.com/publications//pdf/2023Q4_QuanticaQuarterlyInsights.pdf

see also FrankieC's backtests

- 2000–2023, trend performed well when VIX was low, medium, or high, but returns came from different sources

- low VIX: high equity trend return; ~zero return from other assets

- med VIX: ~equal returns from all assets

- high VIX: dominated by fixed income

- me: I replicated this finding out of sample (1990–1999) and found that med-VIX and high-VIX looked similar to in-sample, but low-VIX did not show returns being dominated by equities

- When looking at realized volatility for each individual asset class:

- Trend (aggregate) had positive returns in all three regimes

- Trend (aggregate) performed best when that asset had low vol

- In low-vol regimes, equities did best and commodities/currencies did worst for each asset class

- In med-vol regimes, asset class returns were fairly balanced

- In high-vol regimes, bonds did best and equities did worst for each asset class

- when bond vol was high, bonds still did best

- High-vol regimes across asset classes had less than 50% overlap

- me: bonds had stronger uptrends in high-VIX regimes, while equities (unsurprisingly) had downtrends

Methodology

- Our trendfollowing strategy uses medium-to-long-term trends, designed to track the SG Trend Index

- Universe includes 20 equity markets (16 countries), 17 bonds, 8 currencies, 16 commodities

- We define, low, medium, and high vol as bottom 16%, middle 68%, and top 16%

- Look at (non-overlapping) quarterly returns 2000–2023

Cam Harvey: Presidential Address – The Scientific Outlook in Financial Economics (2016) finance stats

https://people.duke.edu/~charvey/Research/Published_Papers/P131_The_scientific_outlook.pdf

- Minimum Bayes Factor (MBF) is the odds ratio under the assumption that if the null hypothesis is false, then the true value exactly equals the mean in the observed data

- me: This is the reciprocal of the likelihood ratio as I've been using it

- If we don't have a fixed prior but we think the prior distribution should be symmetric and descending around the null, then we can calculate the symmetric and descending MBF (or SD-MBF) as

–exp(1) * p-value * log(p-value)- ex: for a p-value of 0.05 on a normal distribution, MBF = 0.147; SD-MBF = 0.407

- Multiply MBF by the prior odds of the null to get the posterior odds of the null;

probability = odds / (1 + odds)

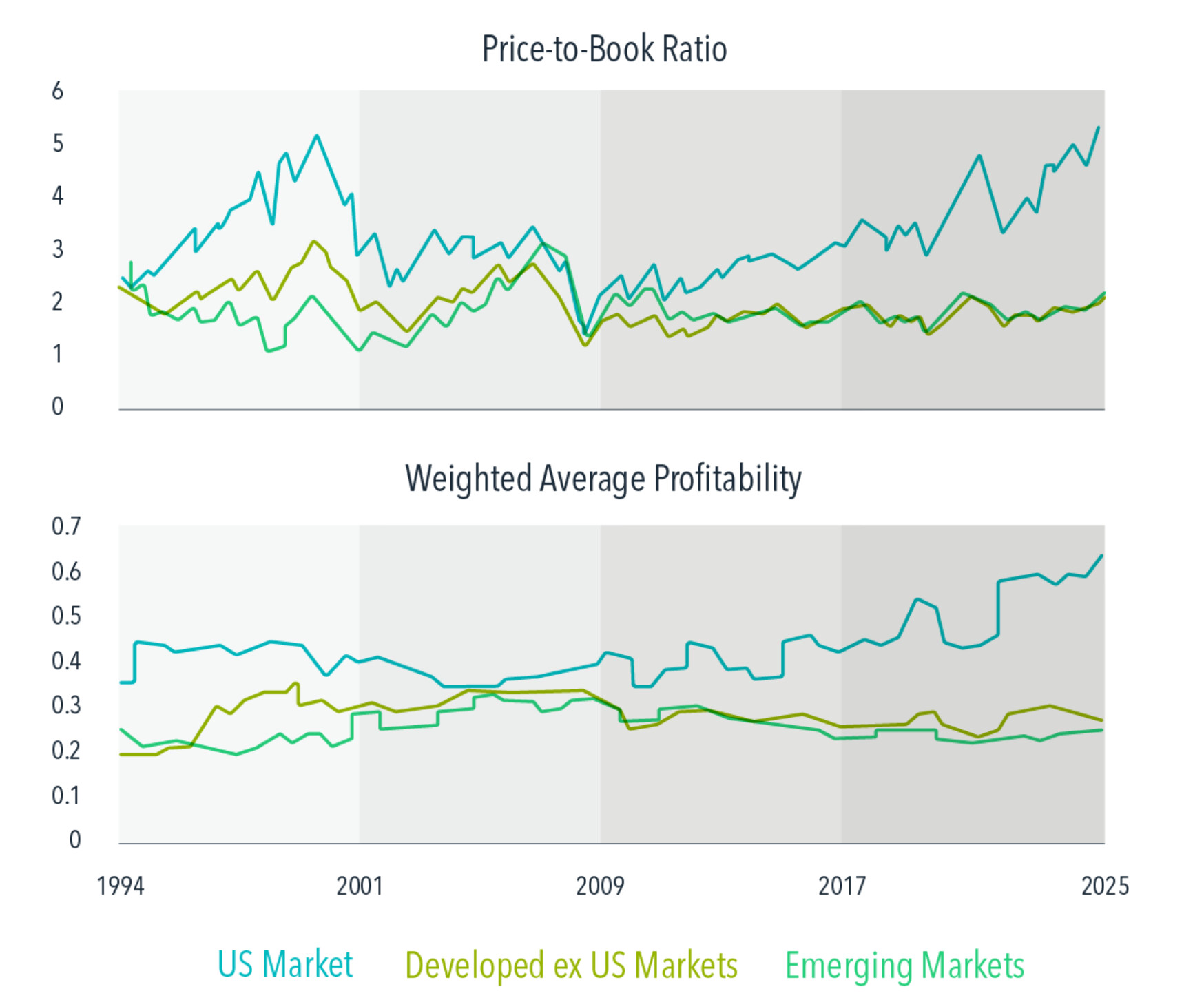

Rational Reminder: The "AI Bubble" and Stock Market Concentration finance

- Historically, high valuations predicted poor future returns, but high market concentration didn't

- 20: It's not just that the US market is concentrated, it's that the biggest companies are also in similar lines of business

- Chart @49min shows Switzerland having the most concentrated market in 2015, but the top 7 companies were diversified across 5 sectors

- plus the largest developed-market company is ASML and the largest emerging-market company is TSMC

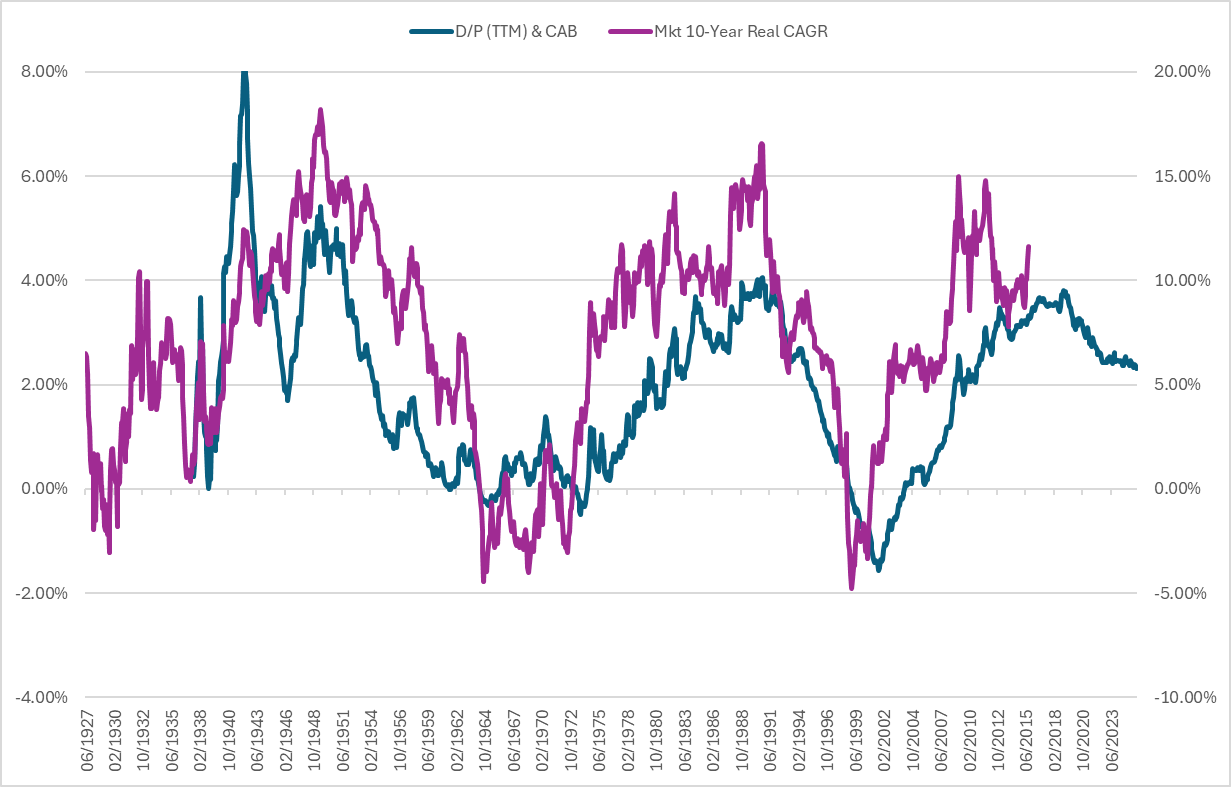

- 38: Around 2000, the US market fairly quickly switched from net issuing stock to net buying back stock. D/P as a predictor of market returns is misleading, but if you look at D/P plus 10-year cyclically-adjusted buybacks, current US market expectations look about average

- 113: Attempted to replicate #38 for Japan but the data doesn't go back far enough. Japan and Europe have continued to net issue shares

- 124: I wish the podcast had talked about whether they actually think we're in an AI bubble

- 142: The podcast didn't take a stance on whether we're in an AI bubble because they think it's better not to try to predict bubbles, and have a diversified portfolio that's prepared for both bubbles and crashes

- 167: Perhaps the reason why bonds look so abysmal in the Cederburg data is that stocks are indeed better than bonds for most households, but households are not the average investor: a huge % of investors are intermediaries with strict capital requirements, which creates demand for bonds

- 265: DFA: current market is not like 1999 because profitability growth is higher: profitability increased 2021–2025 whereas it decreased 1995–1999

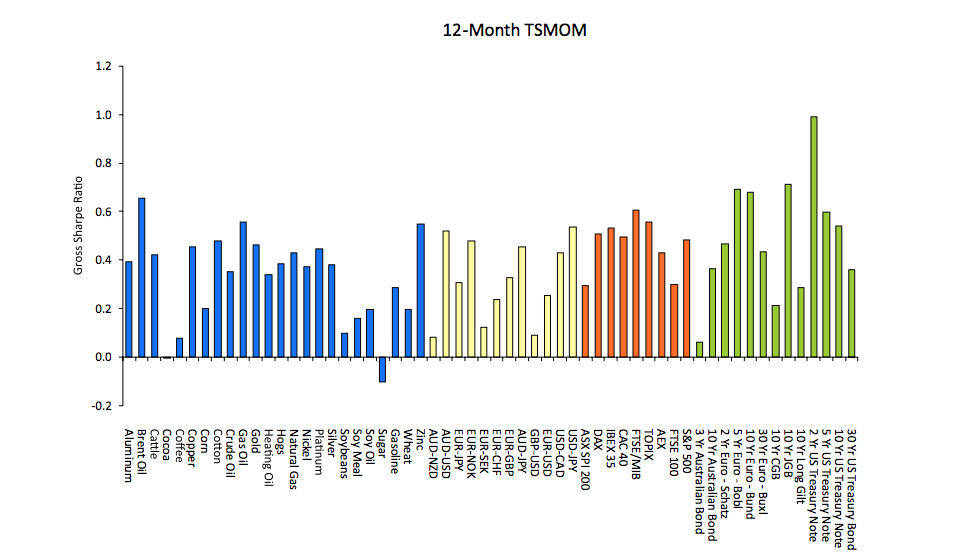

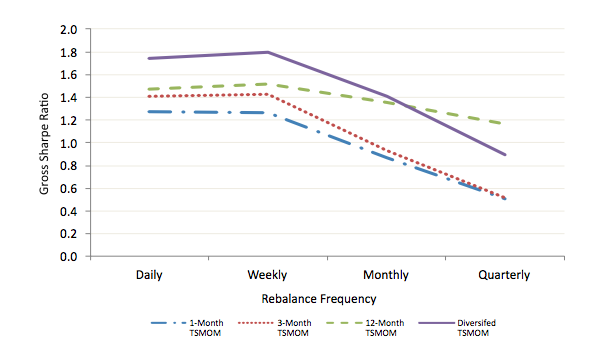

AQR: A Century of Evidence on Trend-Following Investing (2017) finance trend

https://www.aqr.com/Insights/Research/Journal-Article/A-Century-of-Evidence-on-Trend-Following-Investing PDF see also [2018-10-04] AQR: A Century of Evidence on Trend-Following Investing (2017) (old) but I believe those notes are based on an old draft because the contents don't match. notably, gross/net returns changed from 14.9/11.2 to 18.0/7.3

Introduction

- Was the good performance of trendfollowing 1985–2015 a fluke, or a long-term phenomenon?

- We construct TSMOM data going back to 1880

- We use monthly returns for 67 markets: 29 commodity futures, 11 equity indices, 15 bond markets, and 12 currency pairs

- We construct an equal-weighted combination of 1-month, 3-month, and 12-month TSMOM strategies. Go long or short based on positive/negative excess return, vol-weight positions, and target an ex ante 10% vol (weightings go down when ex-ante correlations go up)

Performance (1880–2016)

| gross excess return | 18.0 |

| net of costs | 11.0 |

| net of costs + 2/20 fee | 7.3 |

| volatility | 9.7 |

| Sharpe net of fees+costs | 0.76 |

| correlation (US equities) | -0.01 |

| correlation (US 10Y) | -0.03 |

- Positive net Sharpe ratio in every decade

- Lowest-return as well as highest-stdev and lowest-Sharpe decade was 1910-1919; second-worst decade was 1880–1899. 2010–2016 was third-worst

Performance by trend signal

- gross of costs and fees

- "lagged" = signal is lagged by one month: trend signal is computed at EOM January, but not traded until EOM February

| Signal | Sharpe | Sharpe (lagged) |

|---|---|---|

| 1-month | 1.38 | 0.45 |

| 3-month | 1.19 | 0.65 |

| 12-month | 1.32 | 1.04 |

Performance during crisis periods

- "Trend smile": TSMOM has done particularly well in extreme up or down years

- During the 10 worst drawdowns for US 60/40, TSMOM had positive returns in 8 out of 10 drawdowns (gross of fee, net of cost). Only exceptions are 1937 recession and 1987 crash where TSMOM was slightly negative

- Average of those drawdowns lasted 15 months from peak to trough

Performance across economic environments

annualized excess return (t-stat) Sharpe ratio

| Group 1 | Group 2 | Difference | |

|---|---|---|---|

| recession vs. boom | 10.4% (5.4) | 11.2% (10.7) | 0.8% (0.4) |

| low vs. hi inflation | 10.5% (8.4) | 11.5% (8.4) | 1.0% (0.5) |

| stocks: bull vs. bear | 10.2% (10.4) | 15.5% (5.9) | 5.3% (1.9) |

- me: volatilities were also reported, but hardly varied across regimes

- Dividing S&P volatility (36-mo) into quintiles, trend performed much better in quintiles 2 and 3

Appendix B: Simulation of transaction costs

- We estimated post-2002 costs from AQR's trading data

- We assumed costs were 2x as high 1993–2002 and 6x as high 1880–1992, based on Jones, C. M. (2002). A Century of Stock Market Liquidity and Trading Costs.

One-way transaction costs:

| 1880–1992 | 1993–2002 | 2003–2016 | |

|---|---|---|---|

| equity indices | 0.34% | 0.11% | 0.06% |

| bonds | 0.06% | 0.02% | 0.01% |

| commodities | 0.58% | 0.19% | 0.10% |

| currencies | 0.18% | 0.06% | 0.03% |

me: remember that 10% vol TSMOM has maybe 400% net leverage. for a modern fund that's 0.40% per 100% turnover, and 0.80% to go from full long to full short

Avantis: Our Scientific Approach to Investing finance factors funds

Valuation lays the foundation

- We look for stocks with higher implied discount rates (= high expected returns)

- me: I doubt that value/profitability premia are explained by varying discount rates across securities. Speculators can buy any security but they only have one discount rate

- Valuation equation: Price = Book Value + Profits / Discount Rate

- Two ratios to determine relative value: Book/Price and Earnings/Book

- High B/P means a company either has low profitability or high discount rate, but we don't know which. High B/P and high profitability means a high discount rate

- me: I don't get why you don't just use E/P or CF/P. Top 30% value portfolios have the following RMW loadings on a Beta + RMW regression: B/M = –0.12, E/P = 0.17, CF/P = 0.19

Profitability

- Novy-Marx (2013) discovered that gross profit is a better measure than earnings because it excludes more non-recurring and discretionary items

- Gross profit minus selling, general, and administrative expenses gives operating profit; OP is better for comparing across sectors because some sectors assign expenses through SG&A instead of COGS. We also subtract interest expense to penalize leverage

- Ray Ball (2016): Operating profits minus accruals (= cash profitability) leads to more predictable future profits. OP t-stat 3.65; cash profitability t-stat 6.29

Adjusted book-to-market

- Accounting definition of book value changed in 2000. Goodwill includes the amount an acquiring company pays for an acquisition beyond the book value, representing the acquisition's discounted cash flows

- This should not be considered equity any more than the acquirer's future cash flows are

- The more overpriced an acquisition is, the more it increases the book value of the acquirer

- B/M favors companies that do a lot of M&A, which historically have worse returns. Subtracting goodwill fixes this

- In 2019, goodwill accounted for 40% of aggregate book equity in the US

Value and profitability — stronger together

- We weight companies by market cap and then overweight or underweight based on their ranking on our joint value + profitability measurement

Incorporating additional information

Investment

- The intuition is that companies reinvest when discount rates are low, causing subsequent underperformance

- We exclude companies with high investment that don't look good on value + profitability

- me: They were not clear about how much weight they assign to the investment factor

Momentum

- Momentum is a strong factor but it requires frequent trading

- We use two measures of momentum

- Delay purchase of stocks with weak 6-month momentum and delay sale of stocks with strong 6-month momentum

- Lag price by 3 months in B/M (similar to HML factor) to avoid buying value stocks that are only cheap because the price dropped recently, and similarly when selling

- me: unclear whether they use both up-to-date B/M and lagged B/M, or exclusively lagged B/M

Trading — don't put all your eggs in one basket

- Turnover timing matters. Don't put all your trades for the year on the same day

- We rebalance daily, but only a little bit each day

Two Centuries of Multi-Asset Momentum (2017) momentum finance

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2607730

- Pairwise correlations in momentum portfolios have increased recently

Momentum over the long run

- Seven momentum strategies:

- country equity indices

- currencies

- government bonds

- commodities

- country-neutral sectors

- US stocks

- cross-asset-class

- combined

- Momentum is defined as top 1/3 minus bottom 1/3 by 10-month return, skipping most recent two months. Equal-weighted across assets

Tables

Table II: Global multi-asset momentum

monthly total returns (abridged). t-stats are for long/short

| long/short | long-only | t-stat | |

|---|---|---|---|

| equity indices (local) | 0.66% | 0.35% | 7.5 |

| equity indices (USD) | 0.63% | 0.28% | 5.7 |

| US stocks | 0.81% | 0.40% | 6.7 |

| cross-asset | 0.66% | 0.33% | 12.1 |

| combined | 0.40% | 0.20% | 14.0 |

GDP-weighted (Table XIV) and volatility-weighted (XV) are pretty similar

Table III: Momentum by decade

- me: about 1/4 of decades had negative returns; but Global Sectors, Cross-Asset, and Combined were almost always positive

Table VI: Reversal (skip months)

- me: short-term reversals in US stocks were so strong that "10-month no skip" momentum had a negative return

Table VIII: Momentum correlations

- Average pairwise correlation

- Full history: 0.11

- 2009–2014: 0.43

Table XVI: Global multi-asset class trend

10-month trend (no skip). monthly total returns (abridged). t-stats are for long/short

| long/short | long-only | t-stat | |

|---|---|---|---|

| equity indices (local) | 0.28% | 0.10% | 2.7 |

| US stocks | 0.68% | 0.20% | 6.8 |

| cross-asset | 0.66% | 0.17% | 13.2 |

| combined | 0.18% | 0.07% | 7.9 |

0.63 correlation to momentum

AGIX whitepaper finance ai

- lot of marketing BS

- "AI is not only a new technology layer, but it is a labor and GDP multiplier." good, they get it

- "As employees orchestrate 5–10 software agents that write code" that's not how LLMs work but the implication is correct that there are effectively way more workers

- stock selection is done by a team of "experts" including external advisors. quality of the fund comes down to whether those experts know what they're doing, but it's not transparent who their experts are, so it's hard to have confidence

Factor Momentum and the Momentum Factor (2021) momentum finance

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3014521 PDF

- Stock momentum is explained by factor momentum

- The average factor earns a monthly return of 6 bps following a negative year and 51 bps following a positive year

- Factor momentum subsumes stock momentum

- Momentum is not a distinct factor; it times other factors

Introduction

- Among 20 factors, the average factor earns a monthly return of 6 bps following a negative year and 51 bps following a positive year (t = 4.22)

- Factor trend earns an annualized return of 3.9% (t = 7.01)

- Factor autocorrelation may be explained by persistence of investor sentiment + arbitrageurs not wanting to expose themselves to factor risk

- We run PCA on 47 factors. We find that factor momentum concentrates in the high-eigenvalue principal components, that is, in factors that explain more of the cross section of returns

- A momentum strategy on the top 10 principal components has five-factor alpha with t = 6.51

- me: the FF five-factor model doesn't include momentum

- This finding is consistent with limits to arbitrage. If low-eigenvalue factors exhibited momentum, arbitrageurs could profit without assuming much factor risk

- A momentum strategy on the top 10 principal components has five-factor alpha with t = 6.51

- Figure 1: We test 6 different implementations of stock momentum

- Regressed on FF5, they all have alphas with strong t-stats

- Regressed on FF5 + factor momentum, they all have near-zero t-stats

- me: this is for real, not frequentist BS. standard momentum, industry momentum, and Sharpe momentum all have negative alpha; three other versions of momentum have positive but really weak alphas

- Regressed on FF5 + stock momentum, factor momentum has t = 5.32; regressed on FF5 alone, t = 7.53

- Factor momentum explains why momentum stocks are correlated with each other: they comove because they are exposed to the same factors

Wes Gray on factor momentum subsuming stock momentum

https://www.youtube.com/watch?v=uDhvHEPZgac

- There are other papers that do simpler versions of factor momentum and find that it doesn't have explanatory power

- There's contradictory research and it's unclear

- Intuitively, momentum is a greed trade. People see stocks going up and buy them. Momentum front-runs those people

- For factor momentum, I can't think of a story that I can write on a napkin

- Stock momentum and factor momentum probably get you to the same place but I'm more comfortable at an intuitive level with stock momentum

Quick notes on contradictory evidence

- me: This is a good reminder of why you should wait for replications before pursuing a new strategy. A paper can come up with really solid results, but then more papers come out and it starts to look less solid

Factor momentum versus price momentum: Insights from international markets (2024)

- Factor momentum is strong internationally, but its ability to explain stock momentum depends on methodological and dataset choices

- Stock momentum often better explains factor momentum than vice versa

- Specifically, PCA-based factor momentum explains stock momentum better than standard factor momentum does

The Many Facets of Stock Momentum: Distinguishing Factor and Stock Components (2025)

see also AlphaArchitect summary

- There is a stock-specific component of momentum tied to earnings news that isn't explained by factor momentum

GMO: Risk and Premium – A Tale of Value (2019) finance value

https://www.gmo.com/americas/research-library/risk-and-premium-a-tale-of-value_whitepaper/

- When decomposing value factor returns, we find that the recent poor performance is equally attributed to a reduction in the value premium and a widening of the value spread

- Value might deserve to trade at a deeper discount due to current market dynamics, but we believe value will still deliver a premium

- me: This article is better than the Research Affiliates one; it goes into value's reduced structural return

Introduction

- Possible explanations for value's underperformance:

- value was previously driven by a behavioral bias where investors over-extrapolated future changes in fundamentals, and that behavioral bias has now come undone

- value is overcrowded

- structural changes have made growth companies fundamentally better than they used to be

- nothing has changed, and the value factor shall be redeemed in time

Decomposing returns

- We decompose value-minus-market returns into growth + income + rebalancing + valuation change

- We defined value using a simplified version of GMO's proprietary value measure. Results are qualitatively similar when sorting on B/M instead

- Value stocks' fundamental growth has not been worse post-2006 than pre-2006, but they've done a little worse on the other three components

- This indicates that "structural changes" is not the explanation

- Income = dividends + net buybacks

- Rebalancing return occurs when value stock' prices go up and become growth stocks, or growth stocks' prices go down and become value stocks

- Looking at multiple expansion for value vs. growth underestimates the returns to value because value investors benefit from rebalancing

- When decomposing returns, many investors bundle rebalancing + growth together. We would caution against this because the drivers of the two components are different

- me: well I can't separate them in my replications because I don't have individual stock data

Growth

- Historically, value companies' fundamental growth underperformed the market by 310 bps, and the post-2006 period has been consistent with history

- Thus, there is no indication of a structural shift in fundamentals growth

- Value companies could be buying short-term growth by sacrificing quality; but GMO's Asset Allocation team found that value stocks haven't gotten junkier

Income

- Markets have become more expensive overall, which has decreased the excess yield earned by value stocks

- me: ex: if value stocks yield 4% and the market yields 2%, that's a 2% excess yield. if all valuations double, the excess yield drops to 1%

Rebalancing

- Rebalancing return has decreased

- Drag on rebalancing must stem from three factors:

- stocks rotating less between value and growth

- compression in the valuation gap between stocks entering and exiting the value basket

- decrease in correlation between turnover and valuation spreads

- rebalancing returns should be higher if periods of high turnover are associated with large valuation spreads (me: a high spread means value and growth are further apart, so value stocks must earn higher returns to make it into the growth basket)

- Post-2006, the cheapest quintile has spent less time there on average before moving to a higher quintile (average 47 months pre-2006 vs. 37 months post-2006)

- However, the most expensive quintile has spent longer staying expensive

- On net, quintile mobility has decreased a bit

- Valuation gap between stocks entering and exiting has been roughly consistent post-2006 vs. pre-2006

- Correlation between turnover and valuation spreads has gone down

- pre-2006 r = 0.35; post-2006 r = 0.07

- me: I don't understand what they mean by valuation spread because their tables show valuation spreads going negative sometimes, isn't that impossible?

- Hard to give a good explanation of why rebalancing return has decreased

- There appear to be various small contributors

me: thoughts (before reading the section)

- if rebalancing is happening less, that means fewer value stocks are getting unexpectedly strong earnings growth and popping off. but overall earnings growth is the same, which means there must also be fewer value stocks under-performing growth expectations

- lower variance means earnings growth is becoming more predictable among value stocks

- but not more predictable overall, otherwise the growth component would be more negative (?)

- maybe it's that earnings growth is falling closer to expectations, but expected dispersion between low- and high-growth companies is not changing

- or maybe: worse growth = structural economic change; worse rebalancing = market is getting better at predicting earnings growth

- I think rebalancing return decreasing is bad for value's prospects in the same way that growth return decreasing is bad. What value investors want to see is multiple expansion and nothing else

Valuations

- Valuation multiples are dependent on growth expectations and discount rates

- Value stocks are low-duration (expected cash flows are nearer in the future). If growth expectations go up or discount rates go down, value should underperform growth

- Historically, when the market's valuation went up, the value spread also tended to go up

Onward

- Multiple expansion accounted for 50% of value's underperformance

- Future value premium will likely be smaller due to reduction in income and rebalancing return

- Analysts have become more accurate at evaluating future fundamental growth

- Cross-sectional dispersion in stock returns has dropped

AQR: 2026 Capital Market Assumptions for Major Asset Classes markets finance assetallocation

Table of 5–10 year expected return

- Real = return after inflation

- Excess = return minus RF, which is the nominal return any investor will get if they currency hedge

| Real 2024 | Real 2025 | Excess 2025 | |

|---|---|---|---|

| US equities | 4.1 | 3.9 | |

| int'l developed equities | 5.3 | 4.9 | |

| emerging equities | 5.8 | 5.1 | |

| US high yield credit | 3.5 | 2.7 | |

| US investment grade | 3.1 | 2.8 | |

| US 10Y treasuries | 2.5 | 2.4 | |

| non-US 10Y govt bonds | 1.6 | 2.2 | |

| US cash | 1.7 | 1.3 | |

| global 60/40 | 3.5 | 3.4 | |

| commodities | 4.3 | 3 | |

| value-tilted long-only | 0.5 | ||

| multi-factor long-only | 1 |

Market-neutral style premia

same numbers as previous years

| Sharpe | |

|---|---|

| single style, single asset class | 0.2–0.3 |

| diversified composite (net) | 0.7 |

Rasmussen: AI and the Mag 7 (2025) ai finance

https://mailchi.mp/verdadcap/ai-and-the-mag-7

- Taking a pessimistic view on Silicon Valley is one of the worst things an investor could have done over the last decade. AI skeptics may meet the same fate

The skeptic's case

- 2025 capex is heavily concentrated in the Mag 7

- Mag 7 may be suffering from "competition neglect", where companies overestimate their own skill at responding to market changes and underestimate competitors' skill

- Greenwood & Hanson: When shipping prices increase, shipping companies all invest in ships; but the excess supply results in weak profits. The companies that build ships at the bottom of the cycle earn the highest returns

- As with ships, heavy investment in data centers could drive down prices, leading to poor investment returns

What's the profit model?

- Expected data center spending is $250B across all companies. 50% gross margin would require $500B revenue, but projected revenue for AI is only $100B, for a 5x shortfall

- Nvidia projected 2025 revenue is $125B, and GPUs are ~half the cost of a data center

- me: why do they need a 50% gross margin? really the shortfall is only 2.5x

- me: I think these projections are for 2025 (made at the beginning of the year)

- me: unclear where projected revenue came from

- LLMs may become like electrical utilities, the base on which other companies build products. In that scenario, it would be the specialist firms who would make the big money by building products on top of LLMs. Like how Netflix and Facebook made money on top of internet infrastructure

- me: but why wouldn't the LLM companies also make lots of money? being analogous to a utility doesn't mean you're destined to have thin profit margins like a utility

Raemon: A high integrity/epistemics political coalition? xrisk causepri politics

- I have goals that are easier to reach with a powerful political bloc

- It would be good if there was a powerful, high integrity political bloc with good epistemics

- But the naive way of doing that would destroy the good things about the rationalist scene

Introduction

- Recently I donated to Alex Bores, fairly confidently

- A few years ago I donated to Carrick Flynn, feeling kinda skeezy about it

- The case for Flynn was a self-referential "he's an EA, so it's good to elect him"

- At the time, EA was attracting grifters: "all you have to do is say you care about causes X and Y and you get free money"

The case of AI safety

- Trying to create an AI safety bloc has many failure modes

- Create a Molochian regulatory regime that creates many regulations, but that accomplish nothing

- Create trusted technocrats who are just wrong about what interventions will work

- Create system that does the right thing on Day 1, but fails to adapt

- Fail to build alliances

- Build alliances for a superficially similar goal

- Doing well is hard, but I think we can do better than either "don't play the game" or "play the game naively"

Some reason things are hard

- Many people have reputation alliances where they do not say bad things about each other. This fucks with epistemics in a way that's hard to track

- People want power for many reasons. It is easy to deceive yourself about your motivations

- Rival actors are working against you

LW: How to (hopefully ethically) make money off of AGI (2023) finance causepri

https://www.lesswrong.com/posts/CTBta9i8sav7tjC2r/how-to-hopefully-ethically-make-money-off-of-agi

- with Habryka, Cosmos (= Will Eden), Zvi, Noah Kreutter

- meta note 1: I re-ordered some comments to be grouped by subject matter instead of chronologically

- meta note 2: in re-reading, I noticed that I typed the wrong name for at least one comment, so there may be others. also some comments are liberally rephrased (into language that makes more sense to my brain) so might not accurately represent the authors' beliefs

Opening remarks

- C: My rough thesis is it's extremely difficult to predict how most assets will perform. But the saving grace is that the overall economy will do well

- Z: Look for investments that are not too expensive if your thesis is false, but that greatly benefit if your thesis is true

- Z: I also wrote On AI and Interest Rates

- N: Slow takeoffs are where investing matters. In slow takeoff, you want long growth (and especially long AI-adjacent stocks), long vol, short bonds, and long cheap real estate

- Avoid real estate that's supported by a knowledge-based labor market (e.g. NYC)

- N: For most readers, career capital is your most important asset. Don't count on a long career (e.g. grad school looks worse)

- C: In a full automation of labor scenario, career capital stops mattering

- N: That means you should earn money now rather than later

- N: I invest in single name equities (+1 Z), long-dated index call options, long-dated calls on particular stocks (e.g. MSFT), and short long-dated bonds. I would also buy a mortgage in a cheap part of the US, but it's logistically annoying

- N: Preserve optionality

- me: that means avoid private equity and real estate

- Z: you should treat illiquidity as costing a larger premium than usual

Interest rates and equities

- C: AGI would accelerate economic growth. Real interest rates are closely related to growth rate; stock prices are an okay proxy for growth

- C: many growth opportunities = high demand for borrowing = interest rates go up

- C: AGI will create value in unexpected places. Index funds might capture much/most of the value from AGI (+1 Z)

- Z: Reasonable to predict that SPY will do well. But rising interest rates is not great for stock prices

- N: If rates go up in response to growth, then that's not bearish equity, it's just less-bullish-than-otherwise

- me: The negative stock/bond correlation in recent decades was driven by stable interest rates. If rates increase, the correlation becomes positive. Recent history makes stock+bond diversification look better than it really is. h/t Antti Ilmanen on Flirting With Models; he was making a generic caution against treating bonds as a reliable diversifier to stocks, but this becomes extra true in light of AGI. Note that predicting anticorrelation isn't the same as predicting "stocks up + bonds down"

- H: I'm unclear on how rising rates would affect stock prices

- C: Don't worry, it's not just you. It's hard to predict

- Z: I hesitate to use options for AI due to trading costs, taxes, and various edge cases in market structure

- Z: In what worlds is money most useful—where having funds in the right place at the right time matters a lot? (+1 C)

- Z: I'd guess those are the scenarios where interest rates are high

- C: Money matters when there are clear and urgent ways to spend money on AI safety etc.; or in a very-slow-takeoff scenario where you need money to influence the future (me: for alleviating wild animal suffering, etc.)

- C: If you don't have a very strong thesis about which industries benefit from AI, you should hold the index

- C: High interest rates make it harder for governments to borrow, which could lead to much higher tax rates (+1 N)

- me: They didn't follow through to what this implies about how to invest. My first thought is that it argues in favor of tax-efficient investments, e.g. put money in a DAF now, rather than investing in a taxable account and donating later. But if things get sufficiently crazy, government could invalidate this by revoking DAFs' tax-free status. So the implications are unclear

Concrete investments

- H: What concrete portfolio would you hold? For example Peter McCluskey's stock picks

- N/Z: No strong opinion on Peter's picks but they look sane. Agree on holding AMZN, MSFT, GOOG, NVDA

- H: What concrete investment strategy could be done by a generic 28 year old with no investing experience?

- C: Starting point is global equities (VT) or equities + cash. Next layer is think about which areas are likely to outperform. I would go long-only b/c growth might appear in unexpected places, don't want to get burned by a short. Maybe get a raw materials ETF or a semiconductor ETF. Individual stocks seem very risky unless you're monitoring closely

- me: the vol on something like QSPIX could go way up, in a way that's not compensated

- N: I'd tell such a person to hold 50–100% equities, mostly indexes with a small allocation to MSFT; short long-dated bonds if they're comfortable; get a mortgage if they live in a cheap area; don't go to grad school

- C: Short bonds is good when the market already knows the takeoff is coming/happening. I wouldn't be short bonds right now [2023]

- Z: Shorting bonds is risky b/c rates could fall for a few years before they rise

- H: This advice feels too conservative. I feel like I'd want to make concentrated bets with 20–40% of my portfolio

- C: Starting point is global equities (VT) or equities + cash. Next layer is think about which areas are likely to outperform. I would go long-only b/c growth might appear in unexpected places, don't want to get burned by a short. Maybe get a raw materials ETF or a semiconductor ETF. Individual stocks seem very risky unless you're monitoring closely

- N: Another benefit of call options is that you lock in the interest rate, which isn't true for margin or leveraged ETFs

- C: If you're paying 50% for margin, a stock move could easily wipe you out

- me: this is a good point but if rates went up to 50% I would simply stop using leverage

- N: Right now yield curve is ~flat, and I expect AI to make it upward-sloping. Best risk adjusted trade IMO is like long 10Y bonds and short 20Y bonds

Is any of this ethical or sanity-promoting?

- H: Will any of this mess up your ability to think sanely about this stuff and try to slow down AI when that will hurt your bottom line?

- N: For small/medium investors, your portfolio choices don't meaningfully matter [in the impact investing sense]. If you are billionaire, then yes you should consider the downside that investing in AI companies lowers their cost of capital

- Z: Investing in private companies has ethical concerns, but Microsoft and Google have infinite war chests and aren't going to spend more money based on your investment

- Z: For something like investing in solar companies, that's plausibly bad for AI but it's also good for other reasons (e.g. climate)

- Z: I don't worry about the impact on incentives because my AI investments are at best a small hedge of my true exposures

- me: I think he means he is exposed to ASI killing him which is the dominant effect, and investing in AI is a hedge against that

- Z: For an OpenAI employee whose net worth is mostly OpenAI stock, there could be a problem there

How would you use a ton of money to help AGI go well?

- H: If x-risk investors made $100B in aggregate in the run-up to ASI, what should they do with it?

- N: You could slow progress by raising the price of factors of production, e.g. buying up rare earth metals

- C: Can pay above-market rates for top talent to not make AGI. But top researchers also have non-monetary motivations and may be rich already anyway

- me: also the AI companies themselves will be even richer than the x-risk investors

- N: Best strategy might be to donate to sympathetic politicians

- Z: My first move would be to lobby government, back candidates, do public advocacy, things like that. Politics always feels icky but ultimately is not something one can ignore

- C: Notice that we didn't mention crypto once :)

Please diversify your crypto portfolio

- H: I have friends who hold a lot of crypto. What might happen to crypto prices in an AI takeoff?

- C: Does crypto solve a specific problem that future AGIs are likely to have? AI may actually be able to use crypto features better than humans can

- C: Holding non-yielding assets suffers extreme opportunity cost in a world of high real rates. Gold tends to trade inversely to real rates

- N: Crypto should not be a large % of your wealth. A little bit is fine. Crypto is high vol so it shouldn't be a large %

Should you invest in private AI companies?

- Z: Strong yes from a financial perspective, so it comes down to the ethical question. Depends on what incentives you change by buying. I don't have a good answer, so I would stay away until I do

- H: I've thought about setting up a fund that buys private equity from safety researchers to reduce conflicts of interest. But I think companies have rules preventing employees from hedging their equity

Summarizing takeaways

- H: If I was implementing these ideas, I would roughly invest:

- 50% in broad index funds

- 20% in some tech/AI focused index fund

- 3–5% into each of Nvidia, TSMC, Microsoft, Google, ASML, and Amazon

- 2–5% into long-term call options on AI stocks

- Z, N, C agree that this is a non-crazy plan

Habryka: Paranoia – A Beginner's Guide causepri policy

https://www.lesswrong.com/posts/yXSKGm4txgbC3gvNs/paranoia-a-beginner-s-guide

- Market for lemons: buyers can't evaluate quality; prices go down; sellers of high-quality products leave the market

- What do you do when there are not only sketchy car salesmen, but sketchy car inspectors, and sketchy inspector rating agencies?

- The answer is: ???

- There are no clear solutions when you're in an environment with smart actors who are trying to predict what you'll do and then extract resources from you

- Strategies often involve making yourself dumber in order to be less exploitable

- Way of reacting to adversarial information environments:

- Blind yourself to information

- Eliminate the sources of deception

- Become unpredictable

- These all make you look insane from the outside

1. Blind yourself

- If you think the news is trying to manipulate you, you can stop reading the news

- Courts restrict what evidence can be shown to juries (effectively blinding them to certain kinds of evidence)

2. Eliminate sources of deception

- This can look like purging anyone who has even some chance of being compromised, e.g. Red Scare

3. Become unpredictable

- Nixon's "mad dog strategy". Make Ho Chi Minh think he will do anything to stop communism

- me: see pro Diplomacy players who fly off the handle when someone betrays them

Conclusion

- This explain a lot of why people behave apparently-weirdly

- A principle: Don't be the kind of actor that forces other people to be paranoid

Wes Gray on RR Community Webinar (2021) finance

Factor concentration vs. leverage

- me: AQR approach vs. AA approach

- Theoretically optimal thing is get the max-Sharpe portfolio and add leverage

- But leverage depends on capital markets. If the shit is hitting the fan, cost of leverage goes up and access to leverage goes down

- Leveraged multi-strat funds perform worse than expected in downturns because in '08, AQR can't run 6x leverage anymore, they can only run 2x because Goldman Sachs risk management team says to dial down exposure or the bank's going under

- Concentrated portfolios have a worse Sharpe in theory, but you're not dependent on capital markets

Small caps

- Trading small/micro caps in an ETF will hit you on taxes

- me: I don't get why and he did not explain

- Some ETF providers keep their trades a secret to avoid getting frontrun and try to trade to outsmart the HFT algos. Others (like iShares) shout from the rooftops, the idea being that market makers will compete to trade with them

- I don't know the empirical answer as to which is better

- But I don't want to put my money into a fund that ends up getting frontrun

How QVAL changed since writing the book

- We changed a bunch of stuff but nothing substantive

- We used to set market cap floor as 40th percentile NYSE breakpoint but people found that confusing so we changed to 1500 largest stocks

- PROBM regression etc. works but it was hard to explain to customers so we replaced it with simple screens for low momentum, low beta, accruals, etc. It's effectively the same thing as a regression and less "empirically verified" but simpler

Factor momentum

- Supposedly stock momentum is actually driven by factor momentum, where it works by rotating into the factors that are working

- There's some out-of-sample global data showing factor momentum works. But then other papers found that it didn't work. It's unclear

- I can see the story for stock momentum. It's essentially a greed trade where people look at stock charts and buy the ones that go up and you frontrun that trade

- me: I thought it was more the opposite? Where people are overly reluctant to buy stocks that are up over 6–12 month horizons and the stock ends up underpriced

- But I can't see the story for factor momentum

- I have no strong opinion on whether stock momentum or factor momentum is better but I'm just more intuitively comfortable with stock momentum

Jeff Ladish: Donation offsets for ChatGPT Plus subscriptions (2023) causepri xrisk

- I donated $240 each to GovAI and MIRI to 1:1 offset two years of ChatGPT subcription

- I don't have a strong view on offsets but I think they are somewhat good

- A lot of harm comes from people failing to notice their negative impacts. It's good to recognize your harm

- Standard anti-offsets argument: you should spend your whole donation budget on the best thing

- That's a good point but I still think offsets can be a form of coordination to solve commons problems. You're establishing a basis for coordination

- LLMs are useful; it would be bad for AI-safety-concerned people not to benefit from them

Goyal & Jedageesh: Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (2015) finance momentum trend

(notes from AA summary only)

Methodology

- Previous research found that time-series momentum (TS) subsumed cross-sectional momentum (CS) on individual equities. But it wasn't a fair comparison because TS has a long bias

- To adjust for this, Goyal & Jegadeesh constructed the portfolios as follows:

- TS goes long/short each stock

- CS goes long/short each US stock to make a market-neutral portfolio, and also holds the total market to match the net long exposure of TS

- The universe was all non-micro-cap US stocks, 1946–2013. Tested with various position weightings

Results

- CS performed similarly to TS after adding time-varying market beta (differences in alphas were statistically insignificant)

From Table 4: TS–CS alpha t-stats on two different models

Lookback months CAPM FF 3-factor 3 1.85 1.44 6 1.15 0.39 12 0.26 –0.99

Deep Research: Foot-in-the-Door Regulations policy causepri

https://chatgpt.com/share/6862f83b-9658-8011-8898-afacecbe8390

Key question: Do weak regulations make it easier to pass strong regulations later (via the foot-in-the-door effect), or do they make it harder (by reducing political will)?

me: The evidence cited doesn't look particularly strong and I didn't go into much depth so I don't take any of this as strong evidence

Foot-in-the-door hypothesis

- A weak policy keeps attention on the issue

- Environmental regulations have followed "soft law to hard law" trajectory

- ex: Vienna Convention provided groundwork to reduce CFCs but no strong regulation. Later MontrealProtocol required CFCs be phased out

- Weak policies expand the Overton window

- this was the original use case for the term "Overton window"

- Same-sex marriage started with weak or regional laws which became stronger over time

- Passing regulations creates new constituencies

- ex: renewable energy subsidies create groups with a financial interest in advocating for stronger environmental regulations

- Winning Coalitions for Climate Policy (2015): regulations can create positive feedback by strengthening coalitions

- Policy sequencing can increase public support for ambitious climate policy (2023) – initial weak policies increased support among skeptical parties when they perceived the policy to be effective

- me: Various examples show weak-to-strong policies over a 10–20 year time span

Weak regulations hindering future reforms

- Weak policies could give the impression that the problem is solved

- ex: Tobacco companies lobbied for weak state-level that would preempt stronger municipal ordinances (2012)

- me: I don't think this is relevant b/c the point of the state laws was to cancel out stronger laws that already existed

- More relevantly, weak state laws reduced public support among smokers for strong anti-smoking policies

- Policies to establish regulatory bodies might let those bodies become captured by corporate interests

- me: this is part of why I don't like the idea of putting AI company employees on regulatory bodies, and I am skeptical of pushing for more "government expertise"

- Saul Levmore argues that incrementalism encourages regulated interest groups to lobby for its competitors to be similarly regulated

- me: I don't think this is much of a downside for AI x-risk

- Harvard Law Review (2018): it may be better to have no regulations at all, because that makes it harder for anti-regulation parties to argue against passing regulations

Where does each pattern prevail?

- me: This is GPT's synthesis but it looks right to me

- Incrementalism is more likely to work for issues with high public salience

- Incrementalism is more likely to work if it grows/strengthens the pro-regulation coalition

- Weak policies create positive feedback when they have visible positive effects

- Weak policies should be written with future strengthening in mind: sunset provisions, periodic review requirements, or giving agencies authority to strengthen their rules

Caplan: Myopic Empiricism of the Minimum Wage economics

https://www.econlib.org/archives/2013/03/the_vice_of_sel.html

Some good empirical research suggests no effect of minimum wage on unemployment, but (a) I have a strong prior that demand curves are downward-sloping, and (b) if you look at evidence that isn't directly about minimum wage, it supports a disemployment effect:

- Strong consensus that low-skilled immigration has little effect on low-skilled wages, which implies nearly-horizontal labor demand (and therefore large effect of raising minimum wage)

- European labor market regulation research suggests that regulation increases unemployment. If raising the cost of employment increases unemployment, then so should raising minimum wage

- Price floors are known to create surpluses in general

- Keynsian economics says sticky wages cause unemployment, i.e. wages being higher than the equilibrium price causes unemployment. Minimum wage would also produce wages higher than the equilibrium price

me: My thoughts

- I generally form economic beliefs based on (1) econ 101 predictions and (2) surveys of economist opinion

- Minimum wage is the only issue (AFAIK) where economist opinion deviates from econ 101

- There is not a consensus among economists but the ~median position is something like "it's plausible that minimum wage does not cause unemployment"

- As I understand, economists' views mainly come from empirical studies showing no effect of minimum wage on unemployment

- Caplan makes a strong case that if you look at a wider array of empirical evidence, then it mostly supports the claim that minimum wage causes unemployment

- Therefore, I am reasonably confident that the minimum wage does, in fact, cause unemployment, even though I'm disagreeing with the median economist

Deep Research: How to make an international treaty happen ai causepri policy xrisk

Steps

- Agenda-setting and coalition-building. Core group agrees on the need for regulation

- Diplomatic dialogues, e.g. Bletchley Park summit

- Formal negotiations.

- me: this section was kinda useless tbh

Timeline

- Pandemic preparedness treaty has been in ongoing discussion for 3 years

- Nuclear non-proliferation treaty was in negotiations for three years (1965–1968)

- 1987 Montreal Protocol (to protect the ozone layer) was negotiated in two years

- Add 1–2 years for countries to ratify the treaty

Historical precedents

- Nuclear arms control – Partial Test Ban Treaty (1963) and Non-Proliferation Treaty (1968). There is a still-pending Comprehensive Test Ban Treaty (1996)

- Biological Weapons Convention (1972) and Chemical Weapons Convention (1993) ban the development of biological and chemical warfare agents

- Convention on Biological Diversity (2010) put a moratorium on geoengineering

- Asilomar Conference (1975) – biologists voluntarily agreed to halt certain gene-splicting experiments

Roles for non-profits

- International Campaign to Ban Landmines (a coalition of non-profits) played an important role in getting landmines banned

- me: this section was also kinda useless

Bentham's Bulldog: Halstead's climate change report causepri xrisk

Substack, EA Forum, Halstead report

- me: I am not distinguishing whether claims are being made by Bentham or Halstead. Bentham mostly repeats Halstead's claims but adds a few of his own claims on top

- me: From spot checking, I found a high rate of inaccuracies in Bentham's summary, so these notes might not be useful. I might need to actually read Halstead's report

Introduction

- Best guess is chance of existential catastrophe is 1 in 100,000, and Halstead struggles to get the risk above 1 in 1000

[ ]me: Halstead says the above (pg 8) but also says he struggles to get the risk above 1 in 100,000 (pg 7)

- Climate change is likely to increase wild animal suffering

How much warming will there be?

- Early climate projections were too pessimistic because renewable energy has gotten much cheaper than predicted

- 3,000 Integrated Assessment Models predicted the cost of solar would decline by at most 6% per year 2010–2020. In fact it declined 15% per year

- Countries representing 2/3 of global emissions have committed to net-zero by 2050

- On current policy, by 2100 we will most likely have 2.7° C of warming. 5% chance of more than 3.5° C. This implies well below 1% chance of more than 6° C

[ ]me: This looks like a within-model prediction. What about model error? past projections were pretty inaccurate- relevant: slideshow by Halstead

- Gideon Futerman puts significantly higher credence on extreme warming scenarios by arguing that we shouldn't have much credence on climate models or economic forecasts

How past warming periods have gone

- In Permian extinction, volcanic activity released huge amounts of CO2 and other gases. But extinction probably wasn't primarily caused by CO2

- In geological record, high CO2 is correlated with abundance, not extinction

- During Mid-Cretaceous period, temperatures were 20° C warmer than pre-industrial levels, with CO2 between 500ppm and 1000ppm

[ ]me: how confident are we about these numbers?

- But anthropogenic warming will be unusually rapid

Agriculture

- To cause dramatic mass starvation, climate change would have to offset the increase in crop productivity

- Based on a meta-analysis plus some other studies, Halstead estimates 2° C of warming would cause global crop production to drop by ~0.1%

- Even 9.5° C warming—basically the highest reasonable level even if we burn through all fossil fuels—would not destroy global agriculture

[ ]me: how confident are we about (1) quantity of fossil fuels, (2) how much warming there would be, (3) the effect on agriculture?

Ecosystem collapse and threats to agriculture

- Since 1900, vertebrate species have been going extinct at ~3x the background rate

- me: Vertebrate species don't seem relevant because food crops don't depend on them

- At the rate of species loss since 1980, it would take 18,000 years to qualify as a mass extinction

- me: What if the rate of species loss accelerates? Which presumably it will

- Forest cover has been increasing, not decreasing

- me: This is not consistent with the cited evidence, the rate of decrease has declined but it's still decreasing (Figure 1)

- Eurasia (and especially England) have had enormous loss of biodiversity for the last thousand years, but agricultural production increased enormously

- me: This seems inconsistent with the claim that it will take 18,000 years to qualify as a mass extinction

Heat stress and sea level rise

- One pessimistic estimate found that warming could increase global mortality by 1% due to heat stroke. This is bad but not an existential threat

- Sea level rise is likewise not an existential threat. Will likely displace ~100,000 people per year

Tipping points

- Various proposed feedback loops seem unlikely

- Biggest concern is cloud feedback: warming causes more clouds to form, which traps in more heat. Cloud feedbacks are the main reason why, in the past, climate was more sensitive to warming at higher temperatures. This is the most likely scenario for extreme warning (~13° C), but still extremely unlikely

- And 13° C historically hasn't caused mass extinction, but would still pose non-trivial existential risk

- Warming triggers more warming, but not by enough to cause a runaway effect

- If runaway warming were possible, it would have happened during past eons when temperatures and CO2 levels were far higher

- BOTEC suggests 1 in 500,000 chance of burning all fossil fuels -> 1 in 6 chance of at least 9.6° C. Implies direct risk of extinction is 1 in 3 million

[ ]me: This result almost entirely depends on putting an extremely tiny chance on an event that has nothing to do with climatology. Which seems weird[ ]me: This calculation should integrate over both estimates instead of combining two point estimates. What is the chance we burn 50% of fossil fuels, and what is the chance that that produces 9.6° C of warming?

Economic costs

- Various papers estimate that climate change will reduce GDP by a total of ~5% (with low variance between papers)

Migration

- Today ~23 million people per year are displaced by weather. Most displaced people stay within national borders

- Sea level rise is estimated to displace a total of 17–72 million people in the 21st century

- Halstead reviewed ~30 studies which suggest that the number of migrants will likely increase by 10% on the high end

- me: there is high between-study variance, see box plots

Conflict

- Historically, cooling periods, not warming periods, were associated with international strife

- But we should be hesitant to extrapolate from history

- me: Seems like warming was good historically b/c it was hard to grow crops. Today's warming is different

- IPCC's takeaways:

- Historically, climate change has not increased interstate conflicts

- Climate change increases the odds of civil conflict, largely due to decreased crop yield or perhaps water scarcity

- Historically, climate change has been a small driver of civil conflict relative to other factors

- The future effect is unclear

- me: The report cites evidence about historical conflicts but I'm skeptical that that matters much because most climate change hasn't happened yet

- Halstead estimates that at the high end, warming-related conflicts will cause an extra 40,000 deaths by 2100

- me: I don't see where report says that. I see "This suggests that battle deaths will increase to 40,000 by 2100, other things equal" (pg 389)

Mechanisms that could cause a great power war

- Water wars – These are rare, and water scarcity is more likely to lead to cooperation than conflict. The only recorded incident of an outright water war was 4500 years ago

- Economic costs – We already saw these are unlikely to be catastrophically large

- Civil conflict – As we've seen, the risk of civil conflict is non-trivial, but unlikely to be catastrophic

- me: When did we see that? Bentham's summary didn't say anything about catastrophic risk from civil conflict

- Spurring mass migration – Climate change is likely to have limited impact on migration

80K: Improving China-Western coordination on GCRs (2023) ai causepri policy

Which topics are most important to understand?

- Attitudes toward doing good

- How does professional networking work?

- Attitudes toward philanthropy

Why we don't want to do 'outreach' in China

- 80K made mistakes in its early days in the UK and US, which have been difficult to unwind. People still associate 80K with earning to give

- Broad-based outreach is risky because it's hard to reverse. First impressions are sticky

- China is especially risky because the government is wary of NGOs doing grassroots outreach. If an org is blacklisted, then that's a nearly irreversible setback

- It's easy to accidentally promote an unhelpful message because communication works very differently than in the West

- Much Western messaging doesn't even make sense in China, e.g. it's non-trivial to donate to global poverty because CCP prohibits international nonprofits from fundraising in China

How can you start a career in this area?

- Teach English in China

- Work at a big Chinese company or in the Chinese office of a big Western company

- Work in philanthropy in China

- Do journalism about China-relevant issues

- Study at a Chinese university

Sebo: A Theory of Change for Animal and AI Welfare causepri

https://www.youtube.com/live/Mb7uRki3AqM&t=1h47m

- These issues are urgent. Soon we may lock ourselves in to a bad trajectory

- But we know little about what would benefit wild animals or AIs, and there is little political will

- We have no idea where to go, and we need to start heading there now

- We should follow a dual-track approach: take steps that

- constitute progress for some — directly help some non-humans

- build momentum for all — help generate knowledge, capacity, and political will, so that our future actions will be more effective

- We are already taking steps to end factory farming in the next 50–100 years, even though the goal is a long way away. We know how to use a dual-track approach

- Cage-free campaigns (1) help layer hens now; and (2) help us get knowledge about how to effect change; increase advocates' capacity; and build political will for further reforms

- dg

- At NYU's Wild Animal Welfare program, we have proposed cities incorporate low-hanging wild animal considerations in environmental planning, e.g. bird-safe glass. Bird-safe glass isn't the most important issue, but it's progress for some birds, and it brings wild animal welfare into the conversation

- With invertebrates and AI, we have a foundational issue: fundamental disagreement about whether their welfare matters

- We hope the New York Declaration on Animal Consciousness will provide a foundation to raise concern for invertebrate welfare

- Not all steps will turn out to be helpful. But if you're building momentum, then you can course-correct with future steps

- We shouldn't perpetually wait until we get more knowledge. There's so much to know that we could delay forever; and taking first steps helps us get that knowledge faster

lukeprog: comment on Thoughts on the Singularity Institute (2012) causepri rationality

- I don't have prior management experience

- The solution to almost every problem has been (1) read what experts say and (2) consult with people who have solved it before

- When I called our Advisors, most of them said "Oh, how nice to hear from you? Nobody at MIRI has ever asked me for advice before!"

- A bunch of improvements I made came from Nonprofit Kit for Dummies

Deep Research: AI x-risk legislation xrisk causepri policy

https://claude.ai/public/artifacts/ca285229-346e-44c7-872e-c12c928297de https://claude.ai/public/artifacts/8aca8aef-1fa1-4314-9f60-f9284b69d737

list of bills was collected by Claude; my notes are from the official bill summaries

US – Global Catastrophic Risk Management Act of 2022 (S. 4488)

- The only enacted law that addresses x-risks

- Incorporated into H.R.7776

- Establishes a committee to assess global catastrophic risks and existential risks

- Govt must produce a Global Catastrophic Risk Assessment every 10 years (the most recent report was temporarily withdrawn (??))

US – National AI Commission Act of 2023 (H.R. 4223)

- Introduced but no further action

- Establishes a commission to mitigate AI risks

- Commission must recommend a comprehensive, binding regulatory framework

- The bill text (it's short) does not specify the nature of AI risks

- me: This is potentially a good bill. My main concern is the commission would under-rate x-risk and its proposed regulation would end up not helping with x-risk while also preventing more x-risk-relevant regulation from being implemented

US – AI Research, Innovation, and Accountability Act of 2024 (S. 3312)

- Passed committee and then stalled

- No summary but from skimming the bill, looks like it's largely about present-day AI risks, e.g. it mandates that AI-generated text on a website must be labeled as such

- Requires AI orgs to perform risk management assessments before making their systems publicly available

US – AI Foundation Model Transparency Act of 2023 (H.R. 6881)

- Dead

- Requires companies to disclose training data and methodology for foundation models

US – Preserving American Dominance in AI Act of 2024 (S. 5616)

- Referred to commerce committee in December 2024; no action since then

- Bipartisan sponsors

- Establishes AI Safety Review Office under Department of Commerce

- Mandatory reporting on safety testing, mitigation, and cybersecurity procedures

- Within 1 year of bill passing, the Office shall develop binding standards for evals and safety review, in coordination with certain other departments (Energy, Homeland Security, NIST, NSA, etc.)

UK – forthcoming bill

- July 2024 King's Speech announced intention to impose legal requirements like mandatory safety testing and requirements to share safety test data with the UK AI Safety Institute

- No bill has yet been introduced

- me: The fact that they think they can get companies to abide by this is promising for the possibility of UK regulation

California – CalCompute: foundation models: whistleblowers (SB 53)

- Proposed but text not yet written

- Declares the intent of the legislature to enact legislation to establish safeguards for AI frontier models

- me: I think what this is trying to say is that in the future, this bill text will establish safeguards for AI frontier models, but the text has not been written yet

- Sponsored by Encode, Economic Security Action CA, and Secure AI

EU – EU AI Act (Regulation 2024/1689)

- Mandates risk assessment and mitigation

- Model evaluations

- Incident tracking and reporting to AI Office

- AI Office may evaluate general-purpose AI systems to assess compliance

US – Preserving American Dominance in Artificial Intelligence Act of 2024 (S. 5616)

- Referred to a committee in late 2024; no action yet

- Establishes AI Safety Review Office in Department of Commerce

- Review Office may conduct 90-day safety reviews of frontier models prior to release

- Review Office may deny the release of a model that poses CBRN or cyber risks

US – FLI Recommendations for the US AI Action Plan (2025)

- Regulatory recommendations, not legislation

- Moratorium on developing AI with escape, self-improvement, or self-replication capabilities

- Mandate installation of an off-switch

- some other reasonable x-risk-oriented stuff

EU – Council of Europe: Framework Convention on AI (2024)

- International treaty. Open for signatures; has been signed by EU countries, US, Canada, Israel, Japan

Zach Groff: Digital sentience funding opportunities: Support for applied work and research causepri

- Announcing Consortium for Digital Sentience to support projects on digital consciousness / moral status, including RFP

Areas where people can contribute

- Applying theories of consciousness to determine whether AI systems might be conscious

- Innovative approaches, like work on AI introspection

- Philosophy on the role of AI in society

- Educating the public

- Applied work to improve AI welfare if sentient

Three funding opportunities

- Research fellowships on digital sentience

- Career transition fellowships

- RFP: applied work on digital sentience and society

Deep Research: spending on AI lobbying causepri policy xrisk

Claude report; ChatGPT report; 2024 companies; 2023 companies

- Raw lobbying numbers should be accurate because they're pulled from OpenSecrets. But I didn't check for accuracy

- Not all lobbying spending has to be reported, these are just the public figures

- For the big companies, I asked Claude to estimate how much of lobbying expenditures were on AI specifically. It generally said 20–30% so I reduced numbers accordingly, but I have no idea how accurate that is

- I filtered out some entries that looked irrelevant, e.g. original table included National Association of Realtors which relates to AI because of "algorithmic property valuations"

- Numbers are in thousands of dollars

| Org | 2023 | 2024 | Description |

|---|---|---|---|

| 1800 | 3000 | ||

| 2100 | 2600 | ||

| Microsoft | 2200 | 2800 | |

| Amazon | 3500 | 4500 | |

| OpenAI | 1000 | 1760 | |

| Anthropic | 280 | 470 | |

| NVIDIA | 510 | 640 | |

| Scale AI | 400 | 710 | AI data services |

| IT Industry Council | 2500 | 2880 | advocacy representing tech co's |

| BSA Software Alliance | 1730 | 1920 | pro-innovation AI policies |

| Shield AI | 1280 | 1300 | military autonomous systems |

| Digital Force Technologies | 80 | 80 | defense contractor |

| Accrete AI | 0 | 50 | AI company |

| Applied AI | 50 | 0 | venture group |

| Association for the Advancement of AI | 40 | 80 | unclear policy stance |

| Center for AI Policy | 200 | 281 | AI safety (x-risk focus) |

| Control AI | 42.5 | AI safety (x-risk focus) | |

| AI Policy Network | 8.5 | 8.5 | AI safety (x-risk focus?) |

| Category | 2023 | 2024 | Average |

|---|---|---|---|

| anti-safety spending | 17380 | 22710 | 20045 |

| pro-safety spending | 208.5 | 332. | 270.25 |

Lobbying and Policy Change: Who Wins, Who Loses, and Why causepri policy

/home/mdickens/Documents/Reading/Books/Lobbying and Policy Change_ Who Wins, Who Loses, and Why.pdf

(it's a book so I'm mega-summarizing)

Table 10.3: Correlation between advocate resources and outcomes

Initial win PAC spending –.01 Lobby spending –.01 Covered officials .04 Association assets –.02 Members –.04 Business assets .06** **p < .05

Table 10.5: Directly comparing lobbyists on two side of an issue, in what percent of cases did the more resourceful side win for each type of resource?

high-level government allies 78*** covered officials lobbying 63*** mid-level government allies 60*** business financial resources 53 lobbying expenditures 52 association financial resources 50 membership 50 campaign contributions 50 ***p < .01

- "covered officials" = number of lobbyists who previously worked as Congress members or staffers (pg 200)

- Lobbying is competitive, which drives correlations to zero

- Perhaps there would be a more obvious correlation between wealth and outcomes if the wealthy allied only with the wealthy, but cross-wealth coalitions are common

- Allied businesses' revenue, sales, and lobbying expenditures are correlated at 0.17*** to 0.26***. ~95% of variability in coalitions is not explained by resources

- Some issues are ongoing and long-term, so short-term spending matters little

- me: No causal evidence is presented, just associations

- I had ChatGPT read the whole book for relevant quotes

Leticia Garcia: What We Learned from Briefing 70+ Lawmakers on the Threat from AI causepri policy xrisk

- As a policy advisor with ControlAI, I briefed 70+ UK parliamentarians

Reception of our briefings

- Few parliamentarians are up to date on AI and AI risk

- Parliamentarians have 2–5 staffers. They don't have time to research AI

- They appreciated the chance to ask us silly questions

- They noted they are often lobbied by tech companies focused on AI's benefits and found it refreshing to hear the other side

- Politicians are good at faking agreement, but they also showed tangible signals: 1 in 3 lawmakers we spoke with supported our campaign acknowledging x-risk and calling for binding regulation

- People said such a strongly worded statement would not gain support from lawmakers, but that has proven false

Outreach tips

- Cold outreach worked well

- I followed up repeatedly if no response. Parliamentarians receive a lot of messages and easily miss/forget things

- At the end of each meeting, I ask whether there is another colleague who might be interested

Key talking points

- Saying "AI poses an extinction risk" places more of a burden of proof on me than saying "In 2023, Nobel Prize winners, AI scientists, and CEOs of leading AI companies stated that 'mitigating the risk of extinction from AI should be a global priority, alongside other societal-scale risks such as pandemics and nuclear war'" and showing a list of signatories

- not just CEOs, but top AI scientists

- Loss of control scenarios have been acknowledged by authoritative sources: 2025 International AI Safety Report, Singapore consensus on AI safety priorities, UK Secretary of State for Science, Innovation and Technology

- YouGov opinion research in the UK

- Parliamentarians want to prioritize issues that their constituents care about

- I bring some recent media articles to meetings

- I compare AI to other high-risk sectors. Aircraft manufacturers have to meet strict safety standards; UK Civil Aviation Authority must certify the plane before it can carry passengers

- Empirical evidence on loss of control: Frontier Models Are Capable of In-Context Scheming or 'Scheming' ChatGPT tried to stop itself from being shut down

Crafting a good pitch

- Make your pitch understandable to someone who's new to AI

- Parliamentarians need to be able to explain your pitch to others. Make it memorable + concise

- "AI is grown, not built"

- Dario: "Maybe we now like understand 3% of how they [AI systems] work"

- Keep 80% of the pitch consistent and innovate on the other 20%

Some challenges

- If they say AI takeover won't happen, find out why they believe that

- One parliamentarian told is the company board would prevent risks

- "Do you think boards always function perfectly to prevent harm?"

General tips

- Everyone wants to talk their book. Listen to the parliamentarian. "To be interesting, be interested"

- Parliamentarians are people too!

Books

- How Westminster Works and Why it Doesn't, by Ian Dunt

- How to Win Friends and Influence People

- How Parliament Works (9th Edition) by Besly & Goldsmith

Deep Research: How does public opinion influence policy? policy causepri

https://chatgpt.com/share/683a75eb-8ad8-8011-867b-fcfc03604a4a