Uncorrelated Investments for Altruists

Summary

- Altruists care a lot about finding investments with low correlation to other altruists’ portfolios. [More]

- Altruists can probably decrease correlation by investing in under-utilized asset classes, most notably (1) commodities and (2) long/short equity indexes. [More]

- But there’s a better way to decrease correlation. Some factors—such as value, momentum, and trend—have been shown to predict investment performance. [More]

- We don’t know for sure if these factors will continue to work in the future, but evidence suggests that they will. [More]

- There are publicly-available funds that provide concentrated factor exposure. [More]

- Factor investing is psychologically painful for most people. We can do a few things to mitigate this, but ultimately it seems unavoidable, and this will prevent most people from investing in value/momentum/trend in practice. [More]

Disclaimer: This should not be taken as investment advice. This content is for informational purposes only. Any given portfolio results are hypothetical and do not represent returns achieved by an actual investor.

Cross-posted to the Effective Altruism Forum.

Last updated 2026-01-19.

Contents

- Summary

- Contents

- Why uncorrelated investments?

- Are there uncorrelated asset classes?

- Factor investing

- Uncorrelated investments in practice

- Appendix

- Notes

Why uncorrelated investments?

As a philanthropist, if you have some investments that you plan to donate eventually, then you should be somewhat risk-averse with respect to those investments. When the stock and bond markets go up, you have more money, and you can donate more to charity. But other altruists also have money, and charities receive more funding, so your money isn’t as valuable. Conversely, when markets go down, you have less money to donate at the exact time when charities need funding the most.

You can avoid this by buying uncorrelated investments. If you can find a way to invest that has a low (or even negative) correlation to the overall altruistic portfolio, then there will be times when most altruists lose money, but you gain money, so you can make up for other altruists’ losses. And there will be times where you lose money and others gain money, but you’re not bothered by losing money because other altruists can now provide more funding. (And of course sometimes you’ll gain or lose money at the same time as other altruists, but not as often as if you held stocks and bonds.)

So if you can find an uncorrelated investment with positive expected return, that would be really valuable.

How valuable are uncorrelated investments?

We can use a simple model to get a sense of how much uncorrelated investments matter. Let’s start with the following assumptions:

- Charitable causes have logarithmic utility of money.

- My assets only represent a small percentage of the total altruistic portfolio.

- Altruists all invest in a standard stock/bond portfolio, and use the optimal amount of leverage.

- The unleveraged portfolio has a long-run expected return of 3%, and a standard deviation of 12%.

- I have the ability to invest in an alternative asset with a modest 1% return and 12% standard deviation, but zero correlation to the standard stock/bond portfolio.

- Asset returns follow a log-normal distribution.

The easiest way to think about the value of my portfolio is in terms of the certainty-equivalent interest rate: what guaranteed interest rate would I consider equally as good as this risky portfolio?

Under these assumptions, if I take my portfolio out of stocks/bonds and invest it all in the alternative asset, the new portfolio has a certainty-equivalent excess return of 0.7%.1 If I have $1 million, that means switching to the alternative investment is as good as getting a guaranteed $7,000 per year—and the amount increases as my portfolio grows.

If the alternative asset earns a 3% expected return instead of 1%, switching my portfolio to the alternative asset provides a certainty-equivalent return of 5.9% (!).

And that’s assuming I keep using the same amount of leverage. If I lever up my investment to the point where the overall altruistic portfolio allocates the correct amount to this alternative asset, then I get a certainty-equivalent return of over 300%. (But this requires that I use on the order of 400:1 leverage, which isn’t even remotely realistic.)

This is just an illustrative example, and it’s probably not accurate. The key takeaway is that allocating to uncorrelated investments can potentially provide a lot of value to a portfolio.

Update 2020-12-14: Since originally writing this, I have somewhat changed my views on the significance of uncorrelated investing. I believe that for most altruistic investors in practice, earning higher expected return is more important than decreasing correlation. I explain why in Asset Allocation and Leverage for Altruists with Constraints.

I still believe that, if an altruistic investor can can decrease correlation without sacrificing expected return, then they should. And I still agree with what I wrote in this essay regarding the diversification benefits of different types of investments.

Are there uncorrelated asset classes?

Investors can choose from essentially four asset classes: stocks (a.k.a. equities), bonds, real estate, and commodities. Most people already hold stocks and bonds. Can we get uncorrelated return with real estate and commodities? And can we find under-utilized investments within equities?

(I wrote about most of these in a previous essay. Here, I will go into a little more detail.)

Real estate

For most individual investors, it doesn’t make sense to buy real estate as an investment because it exposes them to too much undiversified risk. But it might make sense for altruists to buy real estate as part of their altruistic investments—this could help diversify the overall altruistic portfolio. Still, there are a few problems with this:

- Most people aren’t rich enough to buy a real estate property as an investment. Even fewer people are rich enough to buy real estate as part of their altruistic investments, i.e., after already investing enough personal money to ensure their financial security.

- If altruists do buy real estate, they should make sure to diversify globally. People who own investment properties tend to buy them in the same city where they live, which makes the property much easier to manage. If effective altruists as a group do this, they will overly concentrate their investments in a few cities where EAs are over-represented, such as Oxford and Berkeley.

You can gain exposure to a basket of real estate investments by buying a REIT, which is a publicly-traded company that earns money primarily by owning real estate. But REITs behave more like stocks than like real estate,2 so they don’t provide the same diversification benefits as direct investments in properties would.

Real estate makes sense as an investment for the extremely wealthy (for example, university endowments often own a lot of land). But it seems like altruists would have a hard time diversifying with real estate, even in the aggregate.

Commodities

Over the past century and a half, commodities have on average produced a positive return on top of the risk-free rate, with fairly low correlation to stocks (r=0.23) and essentially zero correlation to bonds (Levine et al., 2016).34 Commodities aren’t perfectly uncorrelated with a conventional stock/bond portfolio, but they do provide some diversifying power.5

And unlike real estate, commodities are easy to buy. Various ETFs and mutual funds provide exposure to the broad commodities market (as of this writing, the most popular such ETF is PDBC). Commodity funds generally charge higher fees than equity or bond funds, but probably not enough to destroy the commodity return premium.

Startups

As suggested by Paul Christiano:

[I]f you start or invest in a small company, your payoff will depend on that company’s performance (which is typically quite risky but only weakly correlated with the market). […] This special case is only possible because the entrepreneur or investor is putting in their own effort, and moral hazard makes it hard to smooth out all of the risk across a larger pool (though VC funds will invest in many startups). You shouldn’t expect to find a similar situation in investments, except when you are providing insight which you trust but the rest of the market does not (thereby preventing you from insuring against your risk).

Individual companies still tend to move with the market at least somewhat, so for a truly uncorrelated approach, you could invest in the startup while shorting the market.

But note that, at least according to basic theory, you want the overall altruistic portfolio to hold stock in a startup in proportion to the global market portfolio. So if the startup represents 0.0000001% of global wealth, then value-aligned altruists should invest 0.0000001% in that company—which would probably be no more than about $10,000.

Can we find uncorrelated return within equities?

Thanks to home country bias, most investors put too much money in their home countries and not enough into international equities. Effective altruists are over-represented in a few countries like the United States, the UK, and Switzerland. So there might be an opportunity to diversify by over-weighting countries where not many effective altruists live. For example, you could buy an emerging markets index fund like VWO.

But foreign equities are still 80-90% correlated with the domestic market. You can make truly uncorrelated portfolio with a long/short portfolio: buy (go long) emerging markets while shorting domestic equities.

In general, this strategy has an expected return of zero: in the long run, all equity markets should in expectation behave the same on a risk-adjusted basis. But even a zero-expected-return investment might still be a good idea if it decreases the volatility of the overall altruistic portfolio.

But we might have reason to expect some regions of the world to perform better than others. We can fairly reliably predict returns over the span of a decade or so using John Bogle’s expected return formula:

Future Market Returns = Dividend Yield + Earnings Growth +/- Change in P/E Ratio

This formula has a strong theoretical justification, and it has worked well at predicting future returns over the past century (Bogle and Nolan, 20156; Radha, 20207). I won’t go into detail about why this formula makes sense, but for a good layperson’s explanation, see Colby Davis’ Does Reality Even Matter Anymore? Part 1 and Part 2.

Research Affiliates’ Asset Allocation Interactive uses similar methodology to project the 10-year expected return and volatility for a wide variety of asset classes. As of October 2020, it predicts the following expected real returns for various regions:

| US | Europe | Japan | Emerging Markets | |

|---|---|---|---|---|

| Return | 0.2% | 5.2% | 4.5% | 6.9% |

| Standard Deviation | 15% | 19% | 18% | 21% |

According to the Bogle return formula, we can get something like a 6% expected return by going long emerging markets and short US equities (probably closer to 4-5% after costs). And if altruistic investors in general under-weight emerging markets (which I expect they do), then we’re diversifying by doing so.8

We can do a backtest to get a sense of how this regional long/short strategy might look. Over the past 30 years, the US stock market has outperformed the rest of the world. What would have happened if we had bought US equities while shorting international equities?

This backtest doesn’t really tell us how a regional long/short strategy might perform in the future because (1) we’re cheating by picking the best region in hindsight, and (2) emerging market equities tend to be more volatile than developed markets like the US. But it at least tells us how this general type of strategy might perform. (These return figures are nominal, not real, and don’t include fees or transaction costs.)

| US | International | Long US, Short International | |

|---|---|---|---|

| Return | 10.2% | 5.6% | 3.5% |

| Standard Deviation | 14.5% | 16.4% | 11.3% |

If the Bogle return formula is to be believed, investors can earn a positive (in expectation) and uncorrelated return by buying emerging markets while shorting US stocks. Even if we believe the US and emerging markets have similar expected (risk-adjusted) return, most investors under-weight emerging markets, so holding a long emerging/short US equity portfolio could improve the overall altruistic portfolio. (But it could be unpleasant for the investor who knowingly holds a risky investment with zero expected return.)

Factor investing

Some of the asset class strategies identified in the previous section look at least somewhat promising. But we can probably do better.

The best way to get uncorrelated positive return might be to find a gifted investment manager who can beat the market, and then also short the market (or find a manager who gets positive performance with net zero market exposure). But among well-established managers, the best ones don’t want to take your money—they can only maintain their high returns if they keep their list of clients short. (The best investment fund in the world, Renaissance Medallion Fund, caps the fund at $10 billion and doesn’t accept any outside money.) And it’s hard to evaluate managers who don’t have an established track record. I don’t know how a manager without a long track record could produce compelling evidence that they have enough skill to beat the market.9 And if a manager uses a discretionary process, even if they’ve made money in the past, I have no way to know if they will continue to outperform.10

I prefer to focus on strategies that demonstrably work. And the current state of the evidence suggests that the most demonstrably effective way to get uncorrelated return is via factor investing.

What is factor investing?

First, some background. In the sixties, some very smart economists came up with the Capital Asset Pricing Model (CAPM). According to the original formulation of this theory, a stock can only earn a higher expected return if it has greater exposure to market movements. This exposure is called its market beta. When the market moves up or down, a high-beta stock should move up or down even more. And, importantly, there should be no way to predict a stock’s return other than by its exposure to market beta.

But there’s a problem with this theory. In a seminal 1992 paper, Eugene Fama and Kenneth French found11 that they could predict stocks’ returns much more effectively using three factors: market beta, size, and book to market ratio (“value”). In their sample, small companies tended to perform better than CAPM predicted, and so did companies with high book to market ratios. The new Fama-French three-factor model had much greater explanatory power than the CAPM one-factor model.

Later, researchers gathered more evidence on the size and value factors and found that they replicated well out of sample. Additional factors were identified, such as momentum (Jegadeesh and Titman, 199312) and profitability (Fama and French, 200413). Soon, hundreds more papers were published in the quest to identify more factors. Many of these supposed factors failed to replicate, but a few stand out.

What are the factors?

Berkin and Swedroe’s book, Your Complete Guide to Factor-Based Investing, reviews the literature and presents the factors that the authors believe have the strongest supporting evidence and might be worth investing in. To earn its place in the book, a factor must meet five criteria:

Persistent — It holds across long periods of time and different economic regimes.

Pervasive — It holds across countries, regions, sectors, and even asset classes.

Robust — It holds for various definitions (for example, there is a value premium whether it is measured by price-to-book, earnings, cash flow, or sales).

Investable — It holds up not just on paper, but also after considering actual implementation issues, such as trading costs.

Intuitive — There are logical risk-based or behavioral-based explanations for its premium and why it should continue to exist.14

In a book review, Wesley Gray lists the factors from the book with his own assessment of the quality of evidence behind each, ranging from gold to bronze:1516

Market beta: Gold. Pure risk. Legit.

Term Factor: Gold. Pure risk. Legit.

Momentum Factor: Gold. Part risk, part systematic mispricing.

Value Factor: Gold. Part risk, part systematic mispricing.

Trend Following Factor: Gold. Part risk, part systematic mispricing.

Size Factor: Silver. Part risk, maybe part systematic mispricing.

Carry Factor: Silver. Mostly risk, potentially some systematic mispricing.

Profitability & Quality Factors: Bronze. Systematic mispricing? Risk? Unclear. Best used as supplement for size/value factors.

Low-volatility Factor: Bronze. Systematic mispricing? Best used as supplement for size/value/momentum factors.

Default (or credit) Factor: Bronze. Systematic mispricing? Doesn’t pay to own credit risk, historically.

(Gray’s review also includes a list of links for further reading under each factor.)

We already talked about market beta as part of CAPM. The term factor represents the fact that long-term bonds tend to outperform short-term bonds. Almost all investors already expose themselves to these first two factors simply by buying stocks and bonds. If we want uncorrelated investments, we should avoid the market beta and term factors.

Let’s look at the other three factors that Gray identifies as “gold”: momentum, value, and trend.

In brief, what do these factors mean?

- Value: Cheap stocks (as measured by the price-to-book ratio, price-to-earnings, or some other similar metric) tend to outperform expensive stocks.

- Momentum: Assets (such as stocks, bonds, or commodities) with good performance over the past 6-12 months relative to other assets tend to continue to outperform.

- Trend: Assets with good absolute performance over the past 6-12 months tend to continue to perform well.

(To illustrate the difference between momentum and trend: suppose stock A is up 50% over the past 12 months, and stock B is up 10%. The momentum factor would buy stock A and short stock B, because stock A went up more. But the trend factor would buy both, because both went up in absolute terms. Momentum and trend sound similar, but they tend to operate differently enough that they’re worth counting as separate factors—see Factor correlations for a more quantitative justification.)

In practice, investors can use these factors to outperform the market by buying assets that have low valuations/high momentum/positive trend (and maybe also by short-selling expensive/low-momentum/negative-trend assets).

How do we know these factors are real, and not the result of data mining?

In the rest of this section, I will present a series of research papers on the value, momentum, and trend factors, and explain their significance. If you’re already familiar with the research or if you just want to take my word for it that factor investing works, feel free to skip ahead to Uncorrelated investments in practice.

Evidence on factor investing

In 2013, Asness, Moskowitz, and Pedersen published Value and Momentum Everywhere.17 They found that value stocks and momentum stocks outperformed in four different equity markets; and the value and momentum factors had positive returns in country equity indexes, government bonds, currencies, and commodities. They also showed that the performance of value and momentum could not be explained by macroeconomic risk, liquidity risk, or transaction costs.

Geczy and Samonov (2016)18, Baltussen, Swinkels, and van Vliet (2019)19, and Samonov (2020) assembled much longer historical data sets to show that momentum and value have worked for the last two centuries.

Hou, Xue, and Zhang (2017)20 attempted to replicate 447 supposed market anomalies and found that most did not replicate, but the value and momentum factors appeared robust. (The paper did not examine the trend factor.) In a 2017 interview, when asked which factors he expected to still work in 50 years’ time, Zhang said,

I can only speculate what would happen in 2067. I would bet on value, momentum, investment, and [return on equity] (as well as different combinations of these variables).21

The informal article Fact, Fiction and Momentum Investing22 lists some common arguments for why momentum supposedly doesn’t work in practice, and references research explaining why those arguments are wrong. For instance, it cites Trading Costs of Asset Pricing Anomalies23, which used real-world data to show that value and momentum still beat the market after transaction costs. (This study was later extended by Frazzini et al., Trading Costs24, to look at $1.7 trillion of real-world trades, which found “actual trading costs to be an order of magnitude smaller than previous studies suggest”.)

What about the trend factor? Moskowitz, Ooi, and Pedersen’s paper Time Series Momentum25 observed a highly significant (p<0.00001) trendfollowing factor “in equity index, currency, commodity, and bond futures for each of the 58 liquid instruments we consider”, even after controlling for the value and momentum factors. Later papers replicated this finding over a full century of data26 and across 82 previously unstudied securities27.

Why have these factors persisted?

If investors can increase their performance by investing in these factors, why doesn’t everyone invest in them? Why haven’t they been arbitraged away? It’s not entirely clear, but these factors likely persist due to a combination of risk and common behavioral biases (Lakonishok et al., 199328), and limitations on sophisticated investors that prevent them from correcting this mispricing (Lewellen, 201129; Shleifer and Vishny, 199730).

I won’t go into too much detail on the risk vs. behavioral bias question or on the details of the theories behind each. This slide deck summarizes more research on the question. Additionally, Berkin and Swedroe cover this subject in their book, with references to more academic literature.

Will these factors continue to work?

Obviously, we can’t see into the future, and we don’t know if the value, momentum, and trend factors will continue to predict performance. In particular, the value factor has come under scrutiny recently because it has underperformed since about 2007, and trendfollowing has performed poorly over the past decade (at least until the 2020 market crash, where it performed well). How concerned should we be that two out of these three factors haven’t worked well recently?

This recent poor performance is probably due to bad luck. Research on this question supports the idea that these factors will indeed continue to work:

Ilmanen et al. (2019)31 found “little evidence for arbitrage activity influencing returns”.32 That means sophisticated investors are not exploiting these factors to an extent that causes the factors to become less effective. Similarly, according to Blitz (2017)33:

[F]or each factor there are not only funds which offer a large positive exposure, but also funds which offer a large negative exposure toward that factor. On aggregate, all factor exposures turn out to be close to zero, and plain market exposure is all that remains. This finding argues against the concern that factor premiums are rapidly being arbitraged away by investors in [exchange-traded funds].

Lettau et al. (2018)34 found a similar result: in aggregate, mutual funds, ETFs, and hedge funds had negative exposure to the value factor, even among funds that claimed to be “value” funds.

Arnott et al. (2020)35 looked at the value factor in particular, which has had the worst performance in recent years, and concluded that the recent underperformance does not suggest that value no longer works. They reviewed a number of popular explanations for why value investing might not work anymore, and found that while they had some explanatory power, none of them could fully explain value’s recent underperformance. Instead, according to the paper, value investing underperformed primarily because cheap companies became cheaper, and expensive companies became more expensive. Value investing outperforms when undervalued companies revert to reasonable valuations. But recently, undervalued companies have become even more undervalued. That means, in the words of Arnott et al., “the stage is set for potentially historic outperformance of [the value factor] over the coming decade.”

Dan Rasmussen’s 2020 letter An Apology for Small-Cap Value explained value’s recent poor performance in terms of increasing high-yield spreads and valuation spreads, and expressed a similar sentiment to Arnott et al.: “value is uniquely positioned to capitalize on perhaps a once- or twice-in-a-century convergence of opportunities.”

In short: If value investing had stopped working, we would expect to see a narrowing of the valuation spread between cheap and expensive stocks. Instead, the spread has widened, which suggests that, if anything, value will work better in the coming years than it did in the past (although changes in earnings growth could dampen the performance of value).

The 2019 paper You Can’t Always Trend When You Want36 broke down the performance of the trend factor into two components: the existence of trends and the ability of trendfollowing strategies to profit off of them.37 If trendfollowing doesn’t work anymore, we’d expect to see a decrease in trading profit per trend. But profits have been remarkably close to the long-run historical average. Instead, the recent poor performance of trendfollowing is explained by a lack of trends in most markets. The paper found that both the existence of trends and the ability to make money off of them vary over time, and the current period is not particularly unusual.

(Additionally, many investors benchmark their portfolios against the S&P 500, which has performed particularly well over the past decade. So all sorts of diversifying strategies, including not just factors but international equities, bonds, commodities, etc., look bad by comparison.)

Blitz (2011)38 showed that “the theoretically optimal strategic allocation to these [factors] is sizable, even when using highly conservative assumptions regarding their future expected magnitudes.” The optimal portfolio should include tilts toward value, momentum, and trend, even if these factors will only provide slightly positive outperformance going forward. That means if the overall altruistic portfolio has net zero exposure to these factors, altruists on the margin might want to put their entire portfolios into value/momentum/trend, even if the factors have a low expected return (as long as the expected return is positive).

In a 2015 article, How Can a Strategy Everyone Knows About Still Work?,39 Cliff Asness gives some reasons to expect factor investing to continue to work even when it’s well known, and how to think about factors and their expected performance going forward.

For more on this subject, see Berkin and Swedroe, Chapter 8: “Does Publication Reduce the Size of Premiums?”

So the value, momentum, and trend factors can predict asset performance. And although we can’t know for sure, it seems likely that these factors aren’t going away any time soon.

Berkin and Swedroe also identified size, carry, and profitability/quality as factors, and low-volatility and credit as potential factors. The evidence on these isn’t as strong, so let’s focus on the most robust factors: value, momentum, and trend. How can we use these factors to construct an uncorrelated investment portfolio?

Factor correlations

The value and momentum factors, as constructed in the previously-cited paper Value and Momentum Everywhere,17 had nearly zero correlation to the market and negative correlations to each other (r=–0.5). Hurst, Ooi, and Pedersen (2013)40 showed that a simple trendfollowing strategy had close to zero correlation to stocks, bonds, or commodities. According to Time Series Momentum,25 the trend factor was only weakly explained by the market beta, value, and momentum factors (r2=0.3).

As a simple replication with a longer but narrower data set, I used the Ken French data library to look at the correlation between the market beta, value, and momentum factors on US stocks from 1927 to 2019. According to the data, market beta and value had a correlation of r=0.23, market beta and momentum had r=–0.34, while value and momentum had r=–0.41.

Maybe correlation is too technical of a measurement. How does including value, momentum, and trend actually affect the performance of a portfolio? In particular, how do these factors tend to behave when the market performs poorly?

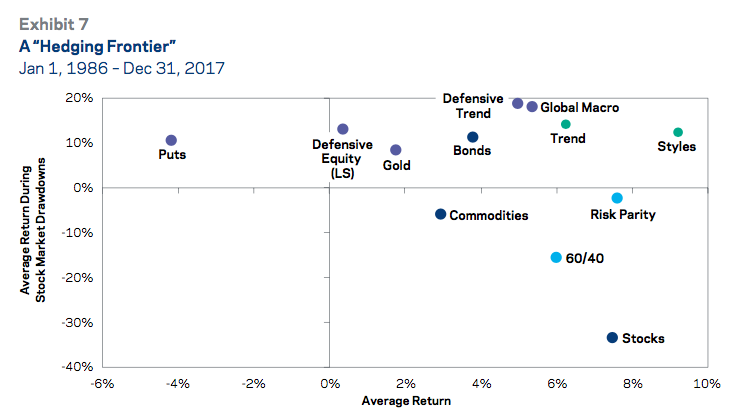

AQR (2018)41 investigated what investments historically provided the biggest benefit during market downturns. It looked at six different investment strategies over the past 90 years to see how they interacted with a stock portfolio both in general and in bad times (plus an additional five strategies over the most recent 30 years). Two strategies stood out as the best: trendfollowing and “styles”—their term for a long/short factor portfolio using value, momentum, and two other factors (carry and low-volatility).

My favorite chart from the AQR report:

If we don’t short individual assets

An academic factor portfolio buys stocks (or other types of assets) that look good according to a particular factor, and short sells assets that look bad. By shorting stocks, we can cancel out the market beta factor: when the market goes up, the long positions rise while the short positions fall (and vice versa), so the fund overall doesn’t move (much). This allows the fund to gain pure exposure to other factors with no exposure to the market.

But short-selling individual stocks can be expensive because you have to borrow the stocks you sell, and short lenders often charge high interest rates. Can we still build a value/momentum portfolio with low correlation to the stock market without shorting?

Let’s do a simple test with the Ken French data library. Instead of investing in the long/short value and momentum factors, what if we invest in the top 10% best value stocks (measured by book-to-market, and equal weighted), as well as the top 10% momentum stocks?

Using data from 1927–2019, the backtest gives the following results for the market, value stocks, and momentum stocks (ignoring fees and transaction costs):42

| Market | Value | Momentum | |

|---|---|---|---|

| Return | 10.0% | 19.4% | 20.0% |

| Standard Deviation | 18.5% | 35.6% | 25.3% |

| Sharpe Ratio | 0.35 | 0.44 | 0.64 |

| Correlation to Market | 1 | 0.75 | 0.84 |

The value and momentum portfolios show impressive performance compared to the market, but unfortunately, they still have pretty high correlation. If we want uncorrelated returns, this doesn’t seem like it will work.

What if instead, as suggested by Alpha Architect, we short the index? We exploit the value or momentum factor on the long side, but on the short side we just hold the market. According to the linked article, we can short a market index for relatively cheap, and they’re more tax-efficient than stocks.

If we take the article’s assumption that the short proceeds equal the risk-free rate minus 0.25 percentage points, then according to the backtest, the long-factor/short-market portfolios performed as follows:43

| Value | Momentum | Combined Val/Mom | |

|---|---|---|---|

| Return | 9.6% | 9.5% | 10.1% |

| Standard Deviation | 24.8% | 13.9% | 16.6% |

| Sharpe Ratio | 0.24 | 0.43 | 0.52 |

| Correlation to Market | 0.34 | 0.21 | 0.34 |

That’s more like it—these portfolios have much lower correlations to the market. We could even get the correlation down to zero by increasing the size of the short position, at the cost of worse return.

Optimized historical portfolios

Nobody knows how factor investing will perform in the future. For illustrative purposes, let’s construct theoretically optimal portfolios under different possible futures and see what they look like.

For simplicity, suppose we have three investment choices: the global equities market, the value factor, and the momentum factor. According to Asness et al. (2013)44, these investments had historical volatilities of 16%, 11%, and 12%, respectively. Both factors had close to zero correlation to the market, and had –0.5 correlation to each other. Let’s assume all these numbers will continue into the future, but make different assumptions about future returns.

If we naively take the historical performance figures from Asness et al., we get about a 5% expected return for the market, 6% for value, and 7% for momentum. Under these assumptions, the optimal portfolio45 allocates 9% to the market, 47% to value, and 44% to momentum.46 Among these three investment options, the optimal historical portfolio contained almost no exposure to the market!

Let’s see what happens if we conservatively assume that the value and momentum factors will return a mere 1% each, while the market return stays at 5%. In this case, the theoretically optimal allocation is 39% to market, 32% to value, and 29% to momentum. Even in this conservative case, the (theoretically) best portfolio still allocates more than half to the value and momentum factors. (Blitz (2011)38 finds a similar result, although it looks at long-only factor portfolios rather than long/short.)

We could try to tightly optimize our factor allocation by projecting future returns and then investing in the optimal portfolio according to our projections. But it’s hard to predict optimal allocations in advance, and equal-weighted portfolios tend to work just as well out of sample (DeMiguel, Garlappi, and Uppal, 200747). So in this example, we could simply allocate 1/3 to the market, 1/3 to value, and 1/3 to momentum.

These simulated examples suggest that the altruistic portfolio should allocate substantial sums to value, momentum, and maybe other factors. Almost no altruists do this. Therefore, it seems plausible that, on the margin, people should allocate 100% of their altruistic investments to long/short factors.

Uncorrelated investments in practice

If we want to move from the land of academia into the real world, we need to deal with some practical considerations:

- How can we actually invest in the value, momentum, and trend factors?

- How can we compensate for our emotions and behavioral biases that make factor investing difficult?

Funds I like

What are some actual investable funds that implement factor strategies like the ones I’ve discussed?

I haven’t spent much time surveying the landscape of funds, and I can’t claim to know which ones are best. If I were investing a lot of money, I’d want to spend much more time learning about what investment options are available and how they work. But it feels unfair of me to talk about factor investing and then not provide any practical suggestions. So as a starting point, I can talk about a few of the funds that I like.

Finding a good factor fund requires a little more than just searching for an ETF or mutual fund with “value” or “momentum” in its name. Many purported value/momentum funds are just index funds in disguise. We want to find funds that provide concentrated factor exposure, not just market beta with a weak tilt.

Astute readers will notice that I’ve cited a lot of papers published by researchers at AQR Capital Management. It sure would be nice if they would use all this great research to build some mutual funds that take advantage of the value, momentum, and trend factors!

Luckily for us, they do exactly that. I briefly reviewed all the mutual funds run by AQR, and based on what I read in the fund documents, I believe two funds give the best exposure to factors with low correlation to stocks and bonds:

- AQR Style Premia Alternative Fund for exposure to value and momentum

- AQR Managed Futures Strategy HV Fund48 for exposure to trendfollowing

(The term “managed futures” can describe a range of investment strategies, but it usually refers to a trendfollowing strategy, as it does in the case of this fund). Buying these two funds together should provide exposure to the value, momentum, and trend factors. AQR Style Premia Alternative Fund also invests in the carry and “defensive”49 factors. I haven’t talked about those factors in this essay because they’re not backed by as much evidence as value/momentum/trend, but allocating some money to them might not be a bad idea. (Notice that these are the same four factors used in the “styles” strategy from AQR (2018)41, cited previously in this essay.)

I found these funds independently of Berkin and Swedroe, but as a corroboration, their book recommends these two funds for combined factor exposure and for trendfollowing exposure, respectively.50

Unluckily for some people, AQR funds have a $1 million minimum investment, so you can’t invest in both these funds unless you have $2 million. (There are three exceptions: (1) you can buy AQR funds in a retirement account with a lower minimum (but it probably doesn’t make sense to keep your altruistic funds in a retirement account); (2) if you live in Australia, you can buy AQR Australia funds with a minimum investment of $25,000; (3) some investment advisors can invest their clients’ money in AQR funds, even if they have less than $1 million.)

But good trendfollowing funds “all pretty much [do] the same thing”, according to Eric Crittenden, former manager of a trendfollowing fund-of-funds.51 I like the KFA Mount Lucas Index Strategy ETF (KMLM),52 which has a lower fee and no minimum investment.

If you want other ideas, this graphic shows the largest trendfollowing managed futures funds as of 2018.

Outside of AQR, it’s a little harder to find a good value or momentum fund with no correlation to the stock market. The investment firm Alpha Architect offers my favorite long-only value and momentum stock ETFs: QVAL, IVAL, QMOM, and IMOM. (Disclosure: I invest in these funds.) I like these funds because they provide much higher factor exposure than most. A more traditional fund such as Vanguard Value ETF provides large exposure to market beta, but only weakly tilts toward the value factor. The Alpha Architect funds are more expensive than Vanguard funds, but they’re just as cheap after adjusting for factor exposure.

The Alpha Architect founders53 have published two books, Quantitative Value and Quantitative Momentum, describing their methodology in detail and explaining why they made the implementation choices that they did. They make some (well-justified) changes to the pure value and momentum factors, incorporating tilts toward quality and low volatility. So their funds may perform a bit better in expectation than a vanilla value or momentum fund (although the main benefit comes from concentrated exposure to the value and momentum factors, not the minor implementation changes). I won’t talk about how exactly these four funds work or why I expect them to outperform “pure” value/momentum, but the books go into lots of detail on this. Alpha Architect has also published two shorter articles summarizing how the funds work: The Quantitative Value Investing Philosophy and The Quantitative Momentum Investing Philosophy.

But these funds are long-only rather than long/short. As we saw previously, long-only equity funds likely have a high correlation to the broad market. According to Alpha Architect’s simulated historical data going back to 1992, an equal-weighted combination of the the four strategies (QVAL/IVAL/QMOM/IMOM) would have had a correlation to the stock market of 0.68.54 But if we bought the Alpha Architect ETFs while shorting market index funds, as discussed previously, the resulting portfolio actually had a negative correlation to the market (r=–0.30). Alpha Architect’s Jack Vogel suggests a similar approach in his article, How to Create a Tax-Efficient Hedge Fund. He proposes buying value/momentum stocks while shorting the S&P 500. He claims that shorting indexes is “much cheaper on an after-cost, after-tax basis for a taxable investor” than shorting individual stocks.

(In practice, it probably doesn’t make sense to go fully market neutral. In theory, the larger your short position, the more leverage you can use, so your expected return doesn’t change; but after considering real-world costs and frictions, increasing the size of the short position reduces expected return. I believe the short side should be around 1/3 to 1/2 as big as the long side, based on an analysis I did here, in which I explain how I derived this estimate.)

I like Alpha Architect’s funds because they provide concentrated factor exposure, and the firm openly discusses the intricate details of their methodology. But unlike the AQR Style Premia Alternative Fund, the Alpha Architect funds only use equities. The AQR fund also uses bonds, commodities, and currencies, so it can probably provide better diversification (although it’s somewhat debatable whether a value/momentum factor fund should include asset classes other than equities). On the other hand, the Alpha Architect funds concentrate in a small number of stocks, which works better for small investors. And ETFs are generally more tax-efficient than mutual funds. Ultimately it’s not clear whether to prefer the AQR Style Premia Alternative Fund or a long/short strategy using the Alpha Architect ETFs, but either choice probably works fine.

This is how I personally would invest my altruistic money, given what I know right now:

- I’d put about half in a long/short strategy where I buy QVAL/IVAL/QMOM/IMOM while shorting a US index fund and an international index fund, with the short position being about 1/3 to 1/2 as large as the long position.

- I’d put the other half in KFA Mount Lucas Index Strategy ETF.55

- I’d use leverage—probably between 2:1 and 3:1.

Update 2020-12-14: I wrote a new essay that goes into more detail on asset allocation: Asset Allocation and Leverage for Altruists with Constraints. See the linked essay for further discussion.

There are many details to consider when making investments in practice, and I can’t cover all of them. If you’re considering building a factor portfolio, do more research or speak to a good investment advisor56 to ensure you understand the implementation details.

I will briefly mention a few such details:

- Different funds will have different tax consequences, which can substantially impact the long-run return of a portfolio.

- Some ETFs, including the Alpha Architect funds, have fairly low volume, so traders must be careful to avoid paying large bid/ask spreads.

- Wealthy investors can ask ETF issuers to issue new shares directly to them, rather than having to buy shares on the open market. This can avert liquidity issues.

- You could pay an investment manager to develop a custom factor portfolio, which might come closer to ideal than the funds I proposed using. (I am sure Alpha Architect would provide this service for a reasonable fee—they already run custom strategies for some clients.) This approach seems especially appealing for extremely wealthy investors.

- Altruists might prefer to use leverage, perhaps a lot of leverage. Investors who want leverage need to decide how to get it.

- Altruists might prefer high-risk, high-return funds, especially if they can’t use leverage. For example, AQR Style Premia Alternative Fund targets 10% volatility, which is low enough that investors who can’t use leverage might prefer to invest in something more volatile.

Behavioral concerns

Factors like value and momentum probably arise from behavioral biases28 that most investors share. People naturally compare their investments’ performance to the performance of the stock market. But a long/short factor portfolio (or really any sort of market-neutral portfolio) can deviate from the market for a decade or more at a time. Almost everyone naturally tracks their performance against the stock market, and doesn’t like to deviate too much. Even long-term-oriented funds such as endowments face heavy criticism after a single bad year. According to a survey by State Street, 40% of institutions would fire a manager after a single bad year, and 89% would fire them after two bad years (more).

Most people don’t actually want zero correlation to the market. We want something that goes up when the market goes down, but that doesn’t go down when the market goes up. (Please let me know if you ever discover such a mythical investment!57)

Factor portfolios are extremely painful. Unless you are an alien.

This raises a practical problem: we’re not aliens. So how do we invest in factor portfolios without giving up when times get tough?

Trendfollowing fund manager Eric Crittenden tells a story about this:

I would show people the calendar-year returns of a managed futures index and let them compare those calendar-year returns to the US stock market and ask them, how would you feel about making a 5% allocation to this managed futures index? And the vast majority of them enthusiastically declined to make an allocation to managed futures. And I said, are you sure? Not even 5%? And they said no way, my clients are gonna fire me, it underperforms, this thing sucks. Why would I do that? I said OK, alright, no problem, let’s kick the managed futures out.

And then I would show them this thing that I call “all-weather” and I didn’t tell them what it was. But between you and me, it’s just a 50/50 split of managed futures and US stocks. But they don’t know. So they do the same thing—they scroll, down they look at the years, and they say, “All right, now we’re talking. This is something I can get behind.” […] And then I reveal to them it’s just a 50/50 split of the thing you kicked out and the thing you [already invest in]—and they’re baffled. Absolutely baffled. To the point where they don’t believe me so I have to give them the spreadsheet and let them look at it and see the math.58

(Crittenden ended up starting a firm that invests in both equities and trendfollowing—much like the 50/50 split he describes.)

This story suggests that the best way to manage our behavioral issues might be to give up on the idea of investing in a strategy that’s totally uncorrelated to the market, and instead do something that’s only partially correlated, such as a mix between trendfollowing/momentum/value and a conventional equity index.

Some more suggestions, taken from talks by Meb Faber59 and Wesley Gray:60

- Create a set of rules and then stick to them. If possible, automate execution—that way, you never have to force yourself to make an uncomfortable trade.

- Share your investing plan with someone who can help hold you accountable.

- Hire an investment advisor to keep you on track/provide behavioral coaching.

- Make sure you understand what you’re investing in and why you expect it to work.

- Study the history of your investment strategy, particularly the times when it’s performed badly. Cliff Asness of AQR has a rule of thumb on what to expect from a strategy during bad times: take the biggest historical drawdown and double it.

The way I think about it: if I’m losing money during a market upswing, then I can’t donate as much. But that’s okay because other altruists will donate more. I don’t think of my altruistic investments as my own money, I think of it as the world’s money. And I’m happy as long as the world gets richer overall.

Ultimately, I don’t believe there’s a great way to overcome our behavioral biases—if there were, factor investing would stop working. But I’m hoping the sort of person who’s crazy enough to donate 10% of their income to cash transfers or AI safety or wild animal welfare is also crazy enough to stick with a weird, unpopular investment portfolio even during bad times.

Appendix

Appendix A: Factors other than value/momentum/trend

In this essay, I focused on value, momentum, and trendfollowing because these are the strongest, most robust factors. But it might make sense to diversify across more than three factors. As shown in Blitz (2011)38 and in my own analysis above, even a factor with only slightly positive expected return should still receive a substantial allocation. That suggests we should invest in as many factors as we can, as long as the factors are reasonably credible.

The funds I listed do include exposure to factors other than value and momentum. AQR Style Premia Fund includes the carry and “defensive” factors; QVAL/IVAL use quality; and QMOM/IMOM use low-volatility.

It might make sense to invest at least a little money in every factor listed by Berkin and Swedroe, with the largest allocations going to the value, momentum, and trend factors. Any alleged factors not included in Berkin and Swedroe’s list probably don’t have strong enough supporting evidence to justify investing in them.

Appendix B: Reducing correlation to income

Technically, we don’t just want to find investments with low correlation to a traditional stock/bond portfolio. Lots of altruists donate money out of their income, so we also want investments not to be correlated with income. In aggregate, income grows with the economy,61 so we want to reduce correlation to economic growth. Can we get that with the value, momentum, and trend factors?

Yes. Sheth and Tim (2017)62 found that the value and momentum factors both performed worse in recessions, but still had positive performance on average. (During recessions, the market had substantially negative performance.) Additionally, during recessions, the pairwise correlations (market, value) and (market, momentum) both dropped below zero, suggesting that they provide even stronger diversification benefits in bad times. In an informal article, Berkin (2020)63 reproduced this result over a longer time horizon.

Hutchinson and O’Brien (2015)64 found a similar result for trendfollowing: it performed worse during recessions than expansions, but still showed positive return during both types of economic environment, and provided diversifying power during downturns. I was able to reproduce this result using AQR’s publicly available time series momentum factor data.65

Appendix C: Changelog

2020-12-04:

- Add a reference to Babu et al. (2020), with explanation.

- Update Funds I like based on some new analysis I’ve done since writing this essay. Previously, I wrote that I personally would invest in a fully market-neutral strategy. I now believe it makes more sense to have some market exposure because beyond a certain point, the cost of short-selling (in terms of reducing expected return) exceeds the diversification benefit.

2021-01-29:

- Update Funds I like to replace AXS Chesapeake Strategy Fund with KFA Mount Lucas Index Strategy ETF (KMLM).

- Change reference to “a forthcoming essay” to link to the actual essay.

2021-02-08:

- Add a reference to Lettau et al. (2018) as a corroboration of Blitz (2017).

2022-05-31:

- Minor wording improvements.

2026-01-19:

- Minor wording improvements.

Notes

-

I performed these calculations using leverage.py, adding the following code:

rra = 1 print(LeverageEnvironment( rra=rra, mu=0.03, sigma=0.12 ).certainty_equivalent_return()) print(LeverageEnvironment( rra=rra, mu=0.9999*0.03 + 0.0001*0.01, sigma=np.sqrt((0.9999*0.12)**2 + (0.0001*0.12)**2) ).certainty_equivalent_return()) -

The linked article primarily reviews a paper: Kizer and Grover (2017). Are REITs a Distinct Asset Class?

It also provides some analysis that’s not covered in Kizer and Grover. ↩

-

Levine, Ooi, Richardson, and Sasseville (2016). Commodities for the Long Run. ↩

-

For interested readers, it is worth noting that commodity futures had positive excess return even while in contango (although returns were higher during times of backwardation, with arithmetic means of 1.8% and 7.7%, respectively). ↩

-

At least according to Levine et al., commodities provide more value when, rather than holding them long-only, we go long on commodity futures in backwardation and short commodities in contango. This is essentially a long/short carry factor strategy. In a later section, I will discuss in more general terms why I believe factor investing makes sense. ↩

-

Bogle and Nolan (2015). Occam’s Razor Redux: Establishing Reasonable Expectations for Financial Market Returns. ↩

-

Radha (2020). Using CAPE to Forecast Country Returns for Designing an International Country Rotation Portfolio. ↩

-

I know we haven’t gotten to the section on factor investing yet, but this strategy is a type of value factor strategy. Emerging equities are cheap and US equities are expensive, so a long/short strategy gains exposure to the value factor while mostly eliminating market beta exposure. ↩

-

Notice that getting uncorrelated positive return and beating the market are equivalent—you can convert one into the other. If a manager beats the market but still has exposure to the market, you can get uncorrelated positive return by shorting the market. And if a manager provides uncorrelated positive return, you can beat the market by investing in both the market and that manager. ↩

-

According to Carhart (1997), On Persistence in Mutual Fund Performance, some mutual funds do persistently beat the market, but their performance is almost entirely explained by their exposure to the size, value, and momentum factors. ↩

-

Fama and French (1992). The Cross-Section of Expected Stock Returns. ↩

-

Jegadeesh and Titman (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. ↩

-

Fama and French (2004). Profitability, Growth, and Average Returns. ↩

-

Introduction, page 24. ↩

-

Quote is edited for brevity. ↩

-

Berkin and Swedroe classify the factors a little differently. They identify seven factors: market beta, term, momentum, value, size, carry, and profitability/quality. They consider trendfollowing a strong investment strategy, but they don’t classify it as a separate factor. They also identify three commonly discussed factors that they don’t believe hold up: dividend yield, low-volatility, and default/credit. Gray does not include dividend yield on his list, presumably because he considers it sub-bronze (I would agree with that assessment).

Berkin and Swedroe acknowledge that trendfollowing has substantial predictive power on top of momentum, so I’m not sure why they don’t consider it a separate factor. ↩

-

Asness, Moskowitz, and Pedersen (2013). Value and Momentum Everywhere. ↩ ↩2

-

Geczy and Samonov (2016). Two Centuries of Price Return Momentum. ↩

-

Baltussen, Swinkels, and van Vliet (2019). Global Factor Premiums. ↩

-

Hou, Xue, and Zhang (2017). Replicating Anomalies. ↩

-

Gray (2017). Want to Learn More About Factor Investing? Read This. ↩

-

Asness, Frazzini, Israel, and Moskowitz (2014). Fact, Fiction and Momentum Investing. ↩

-

Frazzini, Israel, and Moskowitz (2013). Trading Costs of Asset Pricing Anomalies. ↩

-

Frazzini, Israel, and Moskowitz (2018). Trading Costs. ↩

-

Moskowitz, Ooi, and Pedersen (2011). Time Series Momentum. ↩ ↩2

-

Hurst, Ooi, and Pedersen (2017). A Century of Evidence on Trend-Following Investing. ↩

-

Babu, Levine, Ooi, Pedersen, and Stamelos (2018). Trends Everywhere. ↩

-

Lakonishok, Shleifer and Vishny (1993). Contrarian Investment, Extrapolation, and Risk. ↩ ↩2

-

Lewellen (2011). Institutional Investors and the Limits of Arbitrage. ↩

-

Shleifer and Vishny (1997). The Limits of Arbitrage. ↩

-

Ilmanen, Israel, Moskowitz, Thapar, and Wang (2019). How Do Factor Premia Vary Over Time? A Century of Evidence. ↩

-

McLean and Pontiff (2016)66 examined 82 published market anomalies and found that on average, they worked 35% less well post-publication. Ilmanen et al. (2019) re-examined the McLean and Pontiff data along with new pre-sample data and found that the anomalies on average decayed about as much in the pre-sample period as post-sample, suggesting that of the performance decay was attributable to overfitting, not arbitrage by sophisticated investors. They “acknowledge, however, that the power to detect arbitrage crowding into a factor and its effect on prices is challenging […]. For this reason, different tests and different samples may yield different inferences and hence may be why our conclusions differ from Mclean and Pontiff (2016)”.

My own take is that even though the post-sample decays did not statistically significantly differ from the pre-sample decays for any of the tested factors (with the exception of two), the factors did overall perform worse post-sample, which offers Bayesian evidence that arbitrage activity influenced returns (even if only weakly). ↩

-

Blitz (2017). Are Exchange-Traded Funds Harvesting Factor Premiums? ↩

-

Lettau, Ludvigson & Manoel (2018). Characteristics of Mutual Fund Portfolios: Where Are the Value Funds? ↩

-

Arnott, Harvey, Kalesnik, and Linnainmaa (2020). Reports of Value’s Death May Be Greatly Exaggerated. ↩

-

Babu, Levine, Ooi, Schroeder, and Stamelos (2019). You Can’t Always Trend When You Want. ↩

-

Technically, it identified three components, but these two are the relevant ones for our purposes. ↩

-

Blitz (2011). Strategic Allocation to Premiums in the Equity Market. ↩ ↩2 ↩3

-

Asness (2015). How Can a Strategy Everyone Knows About Still Work? ↩

-

Hurst, Ooi, and Pedersen (2013). Demystifying Managed Futures. ↩

-

AQR (2018). It Was the Worst of Times: Diversification During a Century of Drawdowns. ↩ ↩2

-

I used the data series titled “Portfolios Formed on Book-to-Market” and “10 Portfolios Formed on Momentum”. ↩

-

I used the data series titled “Fama/French 3 Factors”, “Portfolios Formed on Book-to-Market”, and “10 Portfolios Formed on Momentum”. ↩

-

Asness, Moskowitz, and Pedersen (2013). Value and Momentum Everywhere. ↩

-

“Optimal” is defined as the allocation that maximizes the Sharpe ratio. ↩

-

DeMiguel, Garlappi, and Uppal (2007). Optimal Versus Naive Diversification: How Inefficient is the 1/N Portfolio Strategy? ↩

-

AQR has two different managed futures funds, the only major difference being that one targets relatively low volatility, and the other targets high vol. Here I linked the high-volatility fund because the expenses are lower on a vol-adjusted basis, and altruists probably prefer higher volatility. ↩

-

In a few papers, AQR defines “defensive” as betting against beta, e.g., Ilmanen et al. (2019).31 Presumably, this fund uses the same definition. The details of the betting-against-beta factor are specified by Frazzini and Pedersen (2013), Betting Against Beta. This is related to the low-volatility factor discussed by Berkin and Swedroe. ↩

-

I originally read their book in 2016, and forgot most of its content. I identified these two AQR funds without any memory of what funds Berkin and Swedroe had recommended. Then, in the process of researching other parts of this essay, I re-read Berkin and Swedroe and saw that they recommended the two funds that I had already listed. ↩

-

Eric Crittenden – All-Weather Portfolios with Trend Following (S3E7). Flirting with Models podcast. 2020. Around 9:30. ↩

-

When this essay was originally published, I wrote that I invested in the AXS Chesapeake Strategy Fund. In February 2021, I moved my investment to KMLM, a new fund that launched shortly after I initially published this essay, primarily because (1) it charges lower fees on a vol-adjusted basis and (2) it’s an ETF instead of a mutual fund, which is more tax-efficient. There exist a few managed futures ETFs with lower fees, but I don’t invest in them because they have too little volatility. Investing in a cheap but low-vol fund means you need to use more leverage, so you end up paying more than if you had invested in the more expensive high-vol fund.

As of 2022, I invest in managed futures through a separately managed account instead of an ETF. But if I did use an ETF, I’d use KMLM. ↩

-

Coincidentally (or perhaps not so coincidentally), both Wesley Gray and Cliff Asness, co-founders of Alpha Architect and AQR respectively, got their PhDs under Eugene Fama—one of the most influential living figures in economics and widely described as the father of the efficient market hypothesis.

Does this prove that, to run a really good asset management firm, you have to study under Eugene Fama? ↩

-

I calculated this by combining Alpha Architect’s data with market data from the Ken French data library, specifically the series titled “Fama/French 3 Factors”. ↩

-

Instead of a 50/50 split, it might be better to use risk parity such that the portfolio is exposed to the same amount of volatility from each of the three factors. ↩

-

Unfortunately, many (most?) investment advisors are kind of clueless, even about basic things like minimizing fees. So it’s important to find a good one. ↩

-

Actually, I do know of an investment like this: Renaissance Technologies’ Medallion Fund. Unfortunately, they won’t accept my money. ↩

-

Eric Crittenden – All-Weather Portfolios with Trend Following (S3E7). Flirting with Models podcast. 2020. Around 54:00. ↩

-

Faber (2020). The Best Investment Opportunity in 40 Years. Interview at the Prime Quadrant conference. ↩

-

Gray (2019). Factor Investing, Simple but Not Easy. ↩

-

Not really, but it’s an okay approximation. ↩

-

Sheth and Tim (2017). Fama-French Factors and Business Cycles. ↩

-

Berkin (2020). Recessions and Factor Performance: What History Tells Us. ↩

-

Hutchinson and O’Brien (2015). Time Series Momentum and Macroeconomic Risk. ↩

-

Time Series Momentum: Factors, Monthly. AQR Data Library. AQR Capital Management, LLC. ↩

-

McLean and Pontiff (2016). Does Academic Research Destroy Stock Return Predictability? ↩